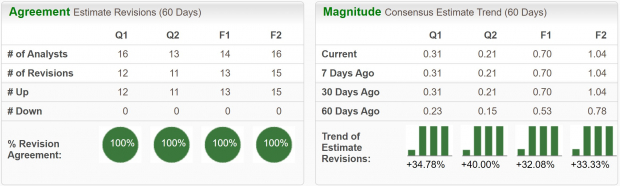

As market participants price in interest rate cuts in 2024, growth stocks like Shopify (SHOP) , are likely to benefit, as investors move further out on the risk curve again.Furthermore, Shopify continues to grow at an impressive pace, with earnings expanding, analysts raising estimates, and a convincing technical setup forms on the chart. For investors looking to add exposure to a high-growth, leading e-commerce platform, Shopify is a worthwhile consideration. Huge Earnings Estimate UpgradesAs the e-commerce megatrend continues, and consumers steadily buy at a healthy pace, top line growth at Shopify is expected to increase nicely over the coming years. FY23 sales are projected to grow 25% YoY to $7 billion, while FY25 is forecast to see growth of 19% YoY to $8.3 billion.Reflecting a strong earnings revisions trend, Shopify boasts a Zacks Rank #1 (Strong Buy) rating. Analysts have unanimously, and significantly increased earnings estimates for SHOP. Current quarter earnings estimates have jumped 35% over the last two months and are expected to climb 342% YoY. FY24 estates have been boosted by 33% and are expected to grow 48% YoY to $1.04 per share.Now that Shopify has divested ownership in its logistics business, which it sold to Flexport, margins should see expansion. The business was outside of the company’s core competencies and thus a drag on profits.  Image Source: Zacks Investment Research Bullish TechnicalsAfter a painful performance in 2022, where many growth-oriented stocks were hammered lower, Shopify has made a major comeback this year. Since the start of 2023, SHOP stock has rallied an impressive 122%.Over the last week, SHOP price action has also been forming a bullish technical momentum pattern, which may send the stock higher to start next year.If Shopify stock can breakout above the $78 level, it would set off a powerful technical buy signal. However, if it can’t hold above the $76 level, the setup would be invalidated and investors may want to wait for another opportunity.

Image Source: Zacks Investment Research Bullish TechnicalsAfter a painful performance in 2022, where many growth-oriented stocks were hammered lower, Shopify has made a major comeback this year. Since the start of 2023, SHOP stock has rallied an impressive 122%.Over the last week, SHOP price action has also been forming a bullish technical momentum pattern, which may send the stock higher to start next year.If Shopify stock can breakout above the $78 level, it would set off a powerful technical buy signal. However, if it can’t hold above the $76 level, the setup would be invalidated and investors may want to wait for another opportunity.  Image Source: TradingView High but Historically Fair ValuationThere is no way around the fact that SHOP trades at a premium valuation, with a forward sales multiple of 14x. However, because of its strong growth trends, and industry positioning, it has always maintained a very high relative valuation.Today, at 14x sales, it is below its five-year median of 22.7x, but is well above the industry average of 5.5x.

Image Source: TradingView High but Historically Fair ValuationThere is no way around the fact that SHOP trades at a premium valuation, with a forward sales multiple of 14x. However, because of its strong growth trends, and industry positioning, it has always maintained a very high relative valuation.Today, at 14x sales, it is below its five-year median of 22.7x, but is well above the industry average of 5.5x.  Image Source: Zacks Investment Research Bottom LineShopify stands as a compelling investment opportunity driven by its robust e-commerce platform, continuous innovation, and adaptability to the evolving digital landscape. In addition to its strong growth rates, the company also maintains a large cash position of $5 billion, giving it considerable flexibility in the coming years.Finally, as Shopify sits in the top 13% (34 out of 251) of the Zacks Industry Rank, broader industry tailwinds adds a market-wide bullish catalyst for the e-commerce juggernaut.More By This Author:Is It Time To Buy Social Media Stocks Going Into 2024? 4 Top-Ranked ETFs Under $20 Up For Gains In 20244 High Earnings Yield Value Stocks To Buy Heading Into 2024

Image Source: Zacks Investment Research Bottom LineShopify stands as a compelling investment opportunity driven by its robust e-commerce platform, continuous innovation, and adaptability to the evolving digital landscape. In addition to its strong growth rates, the company also maintains a large cash position of $5 billion, giving it considerable flexibility in the coming years.Finally, as Shopify sits in the top 13% (34 out of 251) of the Zacks Industry Rank, broader industry tailwinds adds a market-wide bullish catalyst for the e-commerce juggernaut.More By This Author:Is It Time To Buy Social Media Stocks Going Into 2024? 4 Top-Ranked ETFs Under $20 Up For Gains In 20244 High Earnings Yield Value Stocks To Buy Heading Into 2024