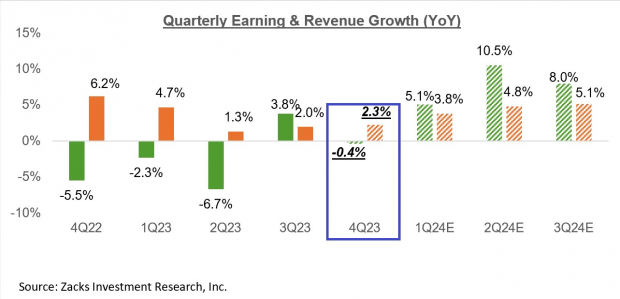

Image: BigstockThe economy’s resilience in the face of the Fed’s extraordinary tightening has been a pleasant surprise. At this time last year, hardly any economists were projecting that the U.S. economy would generate the type of growth momentum that we experienced.That said, it makes sense for growth to moderate going forward to reflect the cumulative effect of monetary policy tightening. However, the earlier higher-for-longer view of interest rates has been modified by the updated Fed outlook that suggests the central bank is getting ready to start easing at some stage in the New Year.All of this has direct earnings implications, as estimates for the coming periods get trimmed.To get a sense of what is currently expected, take a look at the chart below. The chart shows the earnings and revenue growth rates actually achieved in the preceding four quarters, as well as current earnings and revenue growth expectations for the S&P 500 index for 2023 Q4 and the following three quarters.

Image: BigstockThe economy’s resilience in the face of the Fed’s extraordinary tightening has been a pleasant surprise. At this time last year, hardly any economists were projecting that the U.S. economy would generate the type of growth momentum that we experienced.That said, it makes sense for growth to moderate going forward to reflect the cumulative effect of monetary policy tightening. However, the earlier higher-for-longer view of interest rates has been modified by the updated Fed outlook that suggests the central bank is getting ready to start easing at some stage in the New Year.All of this has direct earnings implications, as estimates for the coming periods get trimmed.To get a sense of what is currently expected, take a look at the chart below. The chart shows the earnings and revenue growth rates actually achieved in the preceding four quarters, as well as current earnings and revenue growth expectations for the S&P 500 index for 2023 Q4 and the following three quarters. Image Source: Zacks Investment ResearchAs you can see here, 2022 Q4 earnings are expected to be down -0.4% on +2.3% higher revenues. This follows the +3.8% earnings growth reading in the preceding period (2023 Q3) and three back-to-back quarters of declining earnings before that.This chart, which is an accurate representation of current bottom-up consensus earnings expectations aggregated to the index level, does not see an earnings recession over the next three quarters. If anything, revenue growth is trending up over this period.What we do see in the above chart is the three-quarter period of negative earnings growth from the fourth quarter of 2022 to the second quarter of 2023. Recessions are typically seen as two periods of declining growth. Looking at it this way, the earnings recession issue is in the rear-view mirror at this stage, not something on the horizon.The chart below shows the earnings picture on an annual basis.

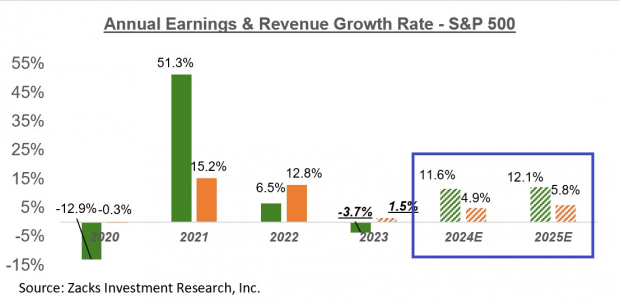

Image Source: Zacks Investment ResearchAs you can see here, 2022 Q4 earnings are expected to be down -0.4% on +2.3% higher revenues. This follows the +3.8% earnings growth reading in the preceding period (2023 Q3) and three back-to-back quarters of declining earnings before that.This chart, which is an accurate representation of current bottom-up consensus earnings expectations aggregated to the index level, does not see an earnings recession over the next three quarters. If anything, revenue growth is trending up over this period.What we do see in the above chart is the three-quarter period of negative earnings growth from the fourth quarter of 2022 to the second quarter of 2023. Recessions are typically seen as two periods of declining growth. Looking at it this way, the earnings recession issue is in the rear-view mirror at this stage, not something on the horizon.The chart below shows the earnings picture on an annual basis. Image Source: Zacks Investment ResearchIt isn’t just the next three quarters where the long-feared recession is missing in action, but actually over the next two years, as you can see above.The earnings recession proponents have been telling us for more than a year that earnings estimates were out-of-sync with the underlying economic reality and needed to be cut in a big way.We did see a period of significant negative estimate revisions that started in April 2022 and lasted for about a year. During that period, estimates in the aggregate declined by about -15% from peak to trough, with the magnitude of negative revisions for several sectors exceeding -20%. These included Construction, Consumer Discretionary, Technology, and Retail.The revisions trend stabilized in April 2023, with earnings estimates for several major sectors, including the Tech sector, going up again. This favorable revisions trend remained in place until October 2023 when estimates started coming down all over again.The chart below shows how earnings growth expectations for the current quarter have evolved since the quarter got underway.

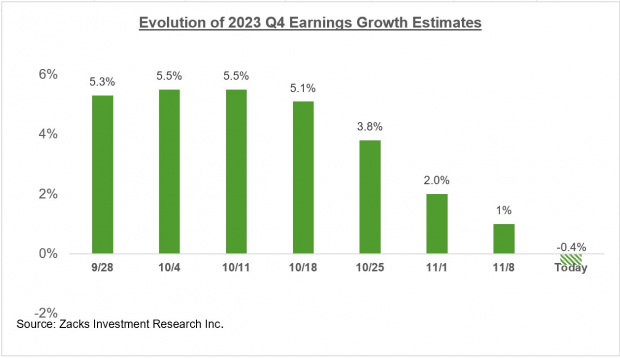

Image Source: Zacks Investment ResearchIt isn’t just the next three quarters where the long-feared recession is missing in action, but actually over the next two years, as you can see above.The earnings recession proponents have been telling us for more than a year that earnings estimates were out-of-sync with the underlying economic reality and needed to be cut in a big way.We did see a period of significant negative estimate revisions that started in April 2022 and lasted for about a year. During that period, estimates in the aggregate declined by about -15% from peak to trough, with the magnitude of negative revisions for several sectors exceeding -20%. These included Construction, Consumer Discretionary, Technology, and Retail.The revisions trend stabilized in April 2023, with earnings estimates for several major sectors, including the Tech sector, going up again. This favorable revisions trend remained in place until October 2023 when estimates started coming down all over again.The chart below shows how earnings growth expectations for the current quarter have evolved since the quarter got underway. Image Source: Zacks Investment ResearchEstimates for full-year 2024 have also been coming down, though the revisions trend appears to have started improving again lately. The chart below shows how the aggregate bottom-up earnings total for 2024 has evolved recently.

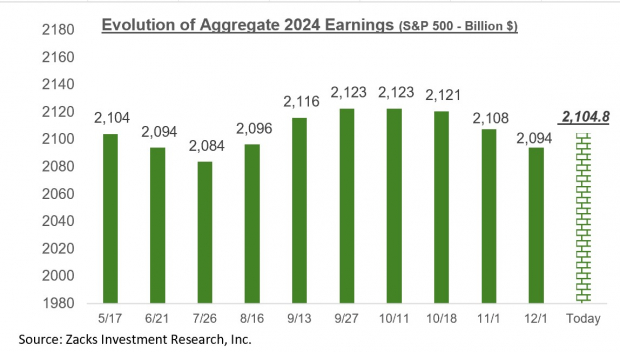

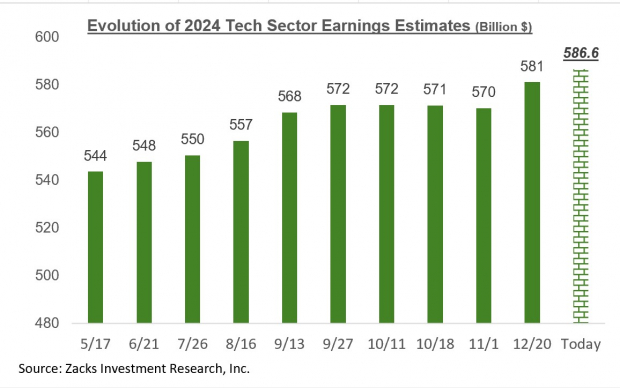

Image Source: Zacks Investment ResearchEstimates for full-year 2024 have also been coming down, though the revisions trend appears to have started improving again lately. The chart below shows how the aggregate bottom-up earnings total for 2024 has evolved recently. Image Source: Zacks Investment ResearchOne sector whose earnings outlook appears to have notably turned around is the Tech sector. This sector has a bigger bearing on the aggregate earnings picture than any of the 15 Zacks sectors in the S&P 500 index, as it is on track to bring in more than 28% of the index’s total earnings over the coming four-quarter period.You can see the recent uptrend in Tech sector estimates in the chart below, which shows the aggregate 2024 earnings estimates for the sector.

Image Source: Zacks Investment ResearchOne sector whose earnings outlook appears to have notably turned around is the Tech sector. This sector has a bigger bearing on the aggregate earnings picture than any of the 15 Zacks sectors in the S&P 500 index, as it is on track to bring in more than 28% of the index’s total earnings over the coming four-quarter period.You can see the recent uptrend in Tech sector estimates in the chart below, which shows the aggregate 2024 earnings estimates for the sector. Image Source: Zacks Investment ResearchOther sectors whose 2024 earnings estimates also appear to have inched up lately include Retail, Autos, Aerospace, and Utilities. While estimates for all the other sectors are still under pressure, sectors facing the most pressure on estimates include Transportation, Industrial Products, and Consumer Discretionary.

Image Source: Zacks Investment ResearchOther sectors whose 2024 earnings estimates also appear to have inched up lately include Retail, Autos, Aerospace, and Utilities. While estimates for all the other sectors are still under pressure, sectors facing the most pressure on estimates include Transportation, Industrial Products, and Consumer Discretionary.

This Week’s Reporting Docket

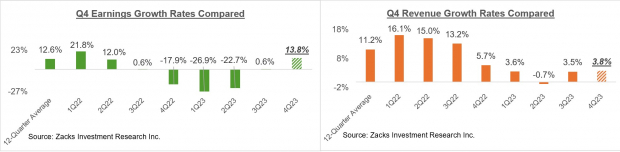

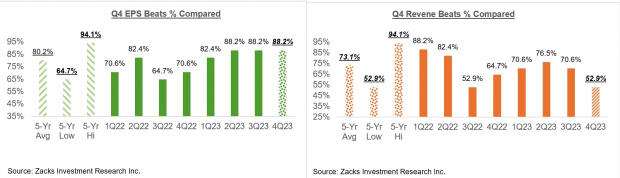

The Q4 reporting cycle will really get going when the big banks start reporting their results on Jan. 12. But the earnings season has actually gotten underway already, with results from 17 S&P 500 members out through Friday, Dec. 29.All of these 17 index members, including bellwethers like FedEx, Nike, Costco, and others, have reported results for their fiscal quarters ending in November. We count all such November-quarter results as part of our December-quarter tally.We have another four S&P 500 members on deck to come out with their fiscal November-quarter results in the first week of the New Year. These include Conagra (CAG – Free Report), Lamb Weston (LW – Free Report), and Walgreens Boots Alliance (WBA – Free Report) on Thursday, Jan. 4, and Constellation Brands (STZ – Free Report) on Friday, Jan. 5. Total earnings for these 17 index members are up +13.8% from the same period last year on +3.8% higher revenues, with 88.2% beating EPS estimates and 52.9% beating revenue estimates.The comparison charts below put the Q4 earnings and revenue growth rates in a historical context. Image Source: Zacks Investment ResearchThe comparison charts below put the Q4 EPS and revenue beats percentages in a historical context.

Image Source: Zacks Investment ResearchThe comparison charts below put the Q4 EPS and revenue beats percentages in a historical context. Image Source: Zacks Investment ResearchThis is way too small a sample of results to draw conclusions about the coming reporting season. However, at this early stage:

Image Source: Zacks Investment ResearchThis is way too small a sample of results to draw conclusions about the coming reporting season. However, at this early stage:

More By This Author:Q4 Earnings Loom: What To Expect Q4 Earnings: What Can Investors Expect?Is An Earnings Recession Coming?