So much for a March rate cut.In our preview of today’s jobs report we quoted Goldman trader John Flood who said that a “hot print was the worst case scenario” (with the whisper number around 190K also well above consensus of 175K), and as if hearing that and eager to make an already ugly week even more painful for traders, moments ago the BLS reporter that in December the US added a whopping 216K jobs, smashing estimates of 175K and coming above all but two of the 67 Wall Street estimates that make up the Bloomberg survey. That said, we are comfortable with predicting that next month today’s print will be revised sharply lower (perhaps even below 175K, meaning today was a miss). Why do we say that? Because once again the BLS revised not just one but both previous months sharply lower:

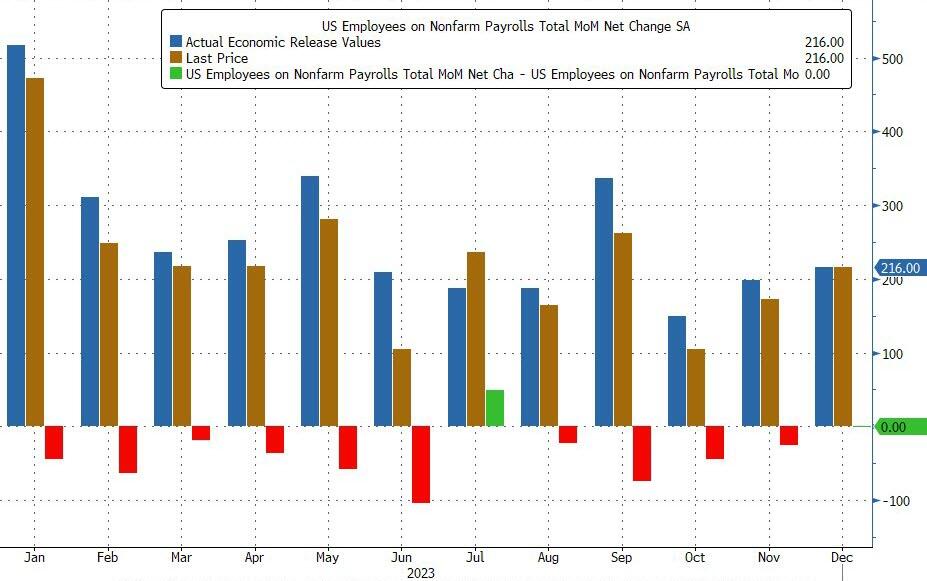

That said, we are comfortable with predicting that next month today’s print will be revised sharply lower (perhaps even below 175K, meaning today was a miss). Why do we say that? Because once again the BLS revised not just one but both previous months sharply lower:

This means that ten of the past 11 jobs reports have been revised substantially lower. And as if the BLS got not a tap on the shoulder, but was being literally Corn-popped by Biden, every other metric came in laughably strong in December, starting with unemployment which remained at 3.7%, missing estimates of a rise to 3.8%. Among the major worker groups, the unemployment rates for adult men (3.5 percent), adult women (3.3 percent), teenagers (11.9 percent), Whites (3.5 percent), Blacks (5.2 percent), Asians (3.1 percent), and Hispanics (5.0 percent) showed little change in December.

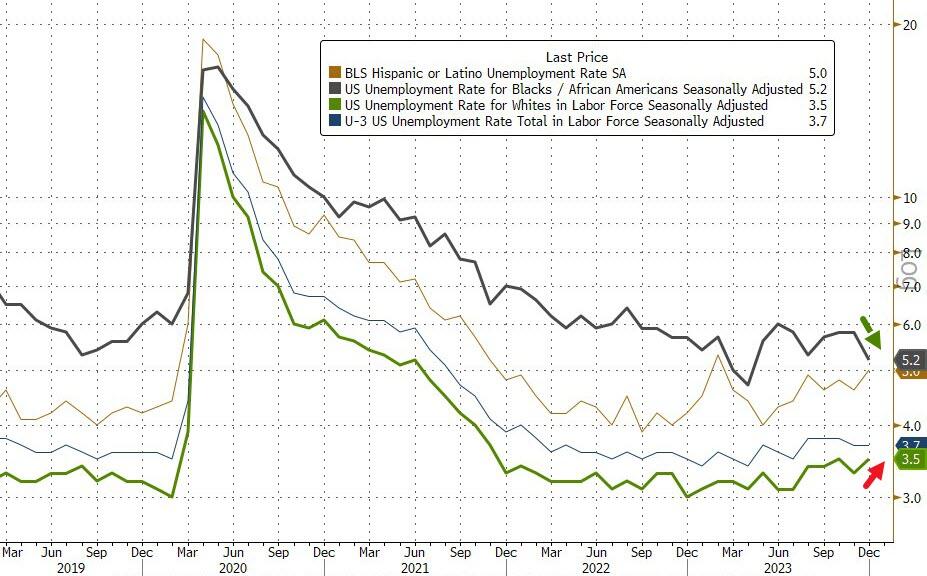

And as if the BLS got not a tap on the shoulder, but was being literally Corn-popped by Biden, every other metric came in laughably strong in December, starting with unemployment which remained at 3.7%, missing estimates of a rise to 3.8%. Among the major worker groups, the unemployment rates for adult men (3.5 percent), adult women (3.3 percent), teenagers (11.9 percent), Whites (3.5 percent), Blacks (5.2 percent), Asians (3.1 percent), and Hispanics (5.0 percent) showed little change in December. Confirming the political nature of today’s report, the unemployment rate among Black workers actually tumbled last month, to 5.2%, down some 0.6 percentage point. White unemployment rose, to 3.5%, up 0.2 percentage point. The usual narrative is that when the labor market starts turning, late in the economic cycle, the Black community is the first and hardest hit. No such indication here.There was some unexpectedly weakness in the labor force participation rate which dropped to 62.5% from 62.8%, missing expectations of an unchanged print. That’s because the number of people not in the labor force soared from 99.695MM to 100.540MM, an 845K increase largely due to a change in historical “data.”

Confirming the political nature of today’s report, the unemployment rate among Black workers actually tumbled last month, to 5.2%, down some 0.6 percentage point. White unemployment rose, to 3.5%, up 0.2 percentage point. The usual narrative is that when the labor market starts turning, late in the economic cycle, the Black community is the first and hardest hit. No such indication here.There was some unexpectedly weakness in the labor force participation rate which dropped to 62.5% from 62.8%, missing expectations of an unchanged print. That’s because the number of people not in the labor force soared from 99.695MM to 100.540MM, an 845K increase largely due to a change in historical “data.” Even more remarkable was that wages, which were expected by many to drop (not us – thank you crazy labor union negotiations), actually came in red hot, as average hourly earnings rose 0.4%, above the 0.3% estimate, and rose to 4.1% from 4.0%, and negating expectations of a decline to 3.9%, as wage growth it appears is here to stay.

Even more remarkable was that wages, which were expected by many to drop (not us – thank you crazy labor union negotiations), actually came in red hot, as average hourly earnings rose 0.4%, above the 0.3% estimate, and rose to 4.1% from 4.0%, and negating expectations of a decline to 3.9%, as wage growth it appears is here to stay. Of course, digging a little deeper in today’s report reveals the usual BLS bullshit – besides just the endless downward revisions of course: consider the usual split between the Household and Establishment surveys: here, while payrolls reportedly increase by 216K (at least until they are revised lower next month), the Household Survey showed a plunge in employment of 683K!

Of course, digging a little deeper in today’s report reveals the usual BLS bullshit – besides just the endless downward revisions of course: consider the usual split between the Household and Establishment surveys: here, while payrolls reportedly increase by 216K (at least until they are revised lower next month), the Household Survey showed a plunge in employment of 683K! Some more details from the report:

Some more details from the report:

Drilling deeper into the breakdown by segment, we find that the now traditional growth led by government, leisure and healthcare… … continued apace:

… continued apace:

Employment showed little change over the month in other major industries, including mining, quarrying, and oil and gas extraction; manufacturing; wholesale trade; information; financial activities; and other services.But the biggest shocker, and one you won’t hear about anywhere else, is that the number of full-time jobs actually plunged by 1.5 million in December to the lowest since Feb 2023, while part-time jobs exploded higher by 762K to the highest on record. And there was another record: in the number of multiple jobholders. We will shortly have a post breaking all of this down.Looking at the market reaction, Bloomberg notes that bond investors got what they were looking for today: a stronger-than-forecast report — including the headline number and a drop in the unemployment rate. Investors are not willing to fade the downtick and instead are sticking with the bearish bias. Yields on 10s traded as high as 4.097% after the data and are not seeing much of a retracement lower. That’s because, with the data in hand, rate-cut odds for March are declining and there is a ton of supply coming. As mentioned Thursday, $110 billion in long-end loaded Treasury supply is slated for the week ahead. Plus, consensus for monthly corporate supply centers on about $160 billion. About $57 billion has already priced. That leaves a lot of supply yet to absorb.That said, once we show just how ugly today’s report actually is, we wonder how long the hawkish reaction will sustain.More By This Author:“Early Signs Of Rebound”: Manhattan Home Prices Rise For First Time In Year’Goldilocks’ Gored By Growth Gains; Bitcoin Bounces As Rate-Cut Hopes HammeredInitial Jobless Claims End 2023 At Year Lows