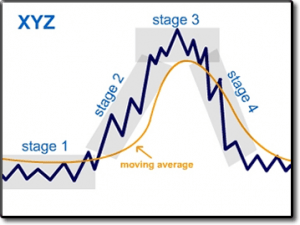

The stock market trading year 2023 is over, and it is time for my financial markets forecast for this coming new year. I noticed that the New York Times last week ran a big story about a popular CNBC talking head and his forecast for big gains for 2024. The story said that he was “correct” in 2023 as he called for bull runs last year when few others did last January. This guy is one of the most frequent CNBC guests and is always bullish. The New York Times story did not note that he was bullish on 2022 too and that turned out to be one of the worst years ever for the 60/40 stocks/bonds portfolio strategy.What the Times story did is give most of its readers what they wanted to hear and that is a rosy prediction for their stocks. And he gives not only the viewers of CNBC, but it’s advertisers what they want to hear too. That may be why Peter Schiff has not been on there for at least twelve months, William Fleckenstein hasn’t been on there for YEARS, and Marc Faber has been banned.I was bearish at the start of 2022 and bullish at the start of 2023.So, let me give you a rundown on what I think about this year when it comes to various markets.Now I always use “stage analysis” to analyze the markets. (For a primer on that get my book Strategic Stock Trading.) Think of markets as being in two cycles.

Think of markets as being in two cycles.

Bonds and the US Stock Market – Let’s start with what is the most important market and that is the bond market, because it impacts all of the others. Bonds go up in value when their yields go down and vice versa. So, when interest rates go up Treasury bonds go down in value. Higher rates means higher costs for companies to finance their debt.The bond market began a secular bull market around 1980, following the inflation of the 1970’s and Paul Volcker’s campaign to stop it with high interest rates. That lasted until 2020 when the Federal Reserve took interest rates down to zero. While interest rates had their cyclical moves higher, after 1980 and before 2020, over time they slowly trended down. That was the secular trend, until they hit zero.Once interest rates hit zero, they had nowhere else to go, but up, and the 10-year Treasury bond made a final all time low on it’s yield at 0.50 in 2020. This is important, because we are not likely to see interest rates go back down to as low as they were in 2020 ever again for the rest of our lives.Nor will the value of bonds, or bond funds, likely ever go up higher than we saw them in the summer of 2020 either.So, the secular trend from that moment forward for bond values is bearish.In 2020, we saw bond funds, such as the ETF TLT, make a stage three top and then fall into their first cyclical bear market, of this new overall bear secular trend for them, in 2022.

This is important, because we are not likely to see interest rates go back down to as low as they were in 2020 ever again for the rest of our lives.Nor will the value of bonds, or bond funds, likely ever go up higher than we saw them in the summer of 2020 either.So, the secular trend from that moment forward for bond values is bearish.In 2020, we saw bond funds, such as the ETF TLT, make a stage three top and then fall into their first cyclical bear market, of this new overall bear secular trend for them, in 2022. The stock market ignored the decline in bond funds in 2021, but then finally rolled over itself and followed bonds down into a bear market of their own in 2022.Stocks made a panic washout in the last quarter of 2022 and then there was a rapid positive shift in the internals of the market in the final weeks of 2022, and first few weeks of 2023, which is what made me turn bullish on the stock market twelve months ago, calling for a cyclical (likely two year) bull market.The bear cycle in the bond market continued, though, last year, as the Federal Reserve continued to raise interest rates. That bear cycle also entered a bit of a panic washout this past September and October as the yield on the 10-year Treasury bond went over 5% and people on CNBC, and in the financial media, began to talk about potential fund problems on the US national debt and a coming sell supply of bonds that will be hard to fill.That moment isn’t here yet, though, but is likely to come as a result of the next US recession.That cyclical bear market for bonds ended this past October with that panic washout. Now bonds are rallying and the Federal Reserve has basically declared that it will not be raising interest rates anymore. The Fed fund futures market is pricing in rate cuts next year, placing the odds as the first one starting in March. Rate cuts are positive for bonds.So, in other words we are now in a cyclical bull market in bonds within a secular bear market. Look for this bull trend in the bond market to last in 2024 and likely continue in 2025.When it ends, though, don’t be shocked if interest rates don’t go up even more than we saw last year on the next Fed hiking cycle.Bond investors need to deal with this NOW.They need to lock in current yields for the next year, maybe two, and at the same time also be wary of another bond bear market after this new bond bull cycle comes to an end.As for the stock market, I still am of the view that the bull market in it for the S&P 500 has limited upside from here, but is not likely to really to begin a new bear market sometime until after the next Presidential election. It could peak in the summer and just float around and do much of nothing. The Federal Reserve is poised to lower rates in part to help Biden – that’s why it has shifted its messaging before they have defeated inflation, thereby abandoning the game plan they put out in the summer of 2022 – which they stated was to keep interest rates elevated with no intention of lowering them, even if a recession came, until inflation truly went away. Jerome Powell put out stories in the Wall Street Journal in 2022 to make it sound like he was going to act like Paul Volcker, but has turned himself into Arthur Burns, who as Chairman in the 1970’s would lower rates during Presidential election years to make whoever was in office happy.The verdict of history:“The only disagreement among economists is whether Burns fully understood the mistakes he was making, or was so wedded to incorrect Keynesian theories that he didn’t realize what he was doing. The only alternative is that he was under irresistible political pressure from Nixon and had no choice. Neither explanation is very favorable to Burns. Economists now recognize the Nixon era as Exhibit A in how the adoption of bad economic policies in pursuit of short-term political gain eventually turns out to be bad politics as well.”

The stock market ignored the decline in bond funds in 2021, but then finally rolled over itself and followed bonds down into a bear market of their own in 2022.Stocks made a panic washout in the last quarter of 2022 and then there was a rapid positive shift in the internals of the market in the final weeks of 2022, and first few weeks of 2023, which is what made me turn bullish on the stock market twelve months ago, calling for a cyclical (likely two year) bull market.The bear cycle in the bond market continued, though, last year, as the Federal Reserve continued to raise interest rates. That bear cycle also entered a bit of a panic washout this past September and October as the yield on the 10-year Treasury bond went over 5% and people on CNBC, and in the financial media, began to talk about potential fund problems on the US national debt and a coming sell supply of bonds that will be hard to fill.That moment isn’t here yet, though, but is likely to come as a result of the next US recession.That cyclical bear market for bonds ended this past October with that panic washout. Now bonds are rallying and the Federal Reserve has basically declared that it will not be raising interest rates anymore. The Fed fund futures market is pricing in rate cuts next year, placing the odds as the first one starting in March. Rate cuts are positive for bonds.So, in other words we are now in a cyclical bull market in bonds within a secular bear market. Look for this bull trend in the bond market to last in 2024 and likely continue in 2025.When it ends, though, don’t be shocked if interest rates don’t go up even more than we saw last year on the next Fed hiking cycle.Bond investors need to deal with this NOW.They need to lock in current yields for the next year, maybe two, and at the same time also be wary of another bond bear market after this new bond bull cycle comes to an end.As for the stock market, I still am of the view that the bull market in it for the S&P 500 has limited upside from here, but is not likely to really to begin a new bear market sometime until after the next Presidential election. It could peak in the summer and just float around and do much of nothing. The Federal Reserve is poised to lower rates in part to help Biden – that’s why it has shifted its messaging before they have defeated inflation, thereby abandoning the game plan they put out in the summer of 2022 – which they stated was to keep interest rates elevated with no intention of lowering them, even if a recession came, until inflation truly went away. Jerome Powell put out stories in the Wall Street Journal in 2022 to make it sound like he was going to act like Paul Volcker, but has turned himself into Arthur Burns, who as Chairman in the 1970’s would lower rates during Presidential election years to make whoever was in office happy.The verdict of history:“The only disagreement among economists is whether Burns fully understood the mistakes he was making, or was so wedded to incorrect Keynesian theories that he didn’t realize what he was doing. The only alternative is that he was under irresistible political pressure from Nixon and had no choice. Neither explanation is very favorable to Burns. Economists now recognize the Nixon era as Exhibit A in how the adoption of bad economic policies in pursuit of short-term political gain eventually turns out to be bad politics as well.” A recession or the next bear market in bonds, is likely to be the next catalyst for the next bear market in the stock market.While I remain bullish for 2024, stocks are risky overall, because their valuations are still sky high.As of today, the Schiller CAPE ratio is sitting at 32.27.When I look at the sectors of the market I’m seeing more bullish setups in the Russell 2000 than the S&P 500 and believe more upside is available in a few select sectors that had panic washouts of their own during the July-October correction of the markets this past year and historically perform well after a peak in an interest rate hiking cycle.Two such sectors are utilities and REIT’s and I bought a few stocks in both those sectors in November.My favorite sector for 2024 is the REIT sector, for which RWR is the most popular ETF.

A recession or the next bear market in bonds, is likely to be the next catalyst for the next bear market in the stock market.While I remain bullish for 2024, stocks are risky overall, because their valuations are still sky high.As of today, the Schiller CAPE ratio is sitting at 32.27.When I look at the sectors of the market I’m seeing more bullish setups in the Russell 2000 than the S&P 500 and believe more upside is available in a few select sectors that had panic washouts of their own during the July-October correction of the markets this past year and historically perform well after a peak in an interest rate hiking cycle.Two such sectors are utilities and REIT’s and I bought a few stocks in both those sectors in November.My favorite sector for 2024 is the REIT sector, for which RWR is the most popular ETF. REIT’s are real estate investment trusts that pay dividends to shareholders.With interest rates peaking, and likely to go down this year and maybe in 2025 too, the yields in various REIT stocks become more attractive to investors.It is important to note that REIT’s and utility stocks tend to perform well in the final innings of an economic growth phrase.And when the final inning is over there is a recession.I’m bullish on gold, silver, and mining stocks.The movements of the US dollar index have the biggest impact on the price of gold and the US dollar tends to go down when interest rates go down, so just based on that gold should do well in 2024, but there is more than just that.

REIT’s are real estate investment trusts that pay dividends to shareholders.With interest rates peaking, and likely to go down this year and maybe in 2025 too, the yields in various REIT stocks become more attractive to investors.It is important to note that REIT’s and utility stocks tend to perform well in the final innings of an economic growth phrase.And when the final inning is over there is a recession.I’m bullish on gold, silver, and mining stocks.The movements of the US dollar index have the biggest impact on the price of gold and the US dollar tends to go down when interest rates go down, so just based on that gold should do well in 2024, but there is more than just that. Gold had a false breakdown last September that coincided with that final spike in the ten year Treasury bond over 5%.That move in bonds brought with it a washout in various markets and that impacted gold.If you take that dip away, gold had been in a trading range between $1900 and $2000 for most of last year – and gold traded in a range while the US dollar index and interest rates went up, which was a positive long-term sign for gold.After that Fall gold dip, and the talk of no more rate hikes from the Fed began, gold took off and went to a new all time high.Things look good for gold now, but I own it for more than just the potential gains it can bring. I also own it in case there are problems in the bond market.So, gold also operates as a hedge against possible future turmoil in the bond market and with the US dollar, that people worried about for a few weeks this past Fall.I don’t think that is going to happen in the next twelve months, as I said, I believe we are now in a short-term cyclical bull market for bonds, but when you are in a secular bear market for bonds at the same time I see gold as a necessary hedge for my bond holdings.And if a time comes when the masses think that too, then it will be too late.These are my big pictures though that are guiding me as we begin this year.More By This Author:The Stock Sectors Now Leading This Rally (Implications For Business Cycle)

Gold had a false breakdown last September that coincided with that final spike in the ten year Treasury bond over 5%.That move in bonds brought with it a washout in various markets and that impacted gold.If you take that dip away, gold had been in a trading range between $1900 and $2000 for most of last year – and gold traded in a range while the US dollar index and interest rates went up, which was a positive long-term sign for gold.After that Fall gold dip, and the talk of no more rate hikes from the Fed began, gold took off and went to a new all time high.Things look good for gold now, but I own it for more than just the potential gains it can bring. I also own it in case there are problems in the bond market.So, gold also operates as a hedge against possible future turmoil in the bond market and with the US dollar, that people worried about for a few weeks this past Fall.I don’t think that is going to happen in the next twelve months, as I said, I believe we are now in a short-term cyclical bull market for bonds, but when you are in a secular bear market for bonds at the same time I see gold as a necessary hedge for my bond holdings.And if a time comes when the masses think that too, then it will be too late.These are my big pictures though that are guiding me as we begin this year.More By This Author:The Stock Sectors Now Leading This Rally (Implications For Business Cycle)

Silver Looks Ready To Shine As The US Dollar Index Rolls Over

My Stock Market Outlook For The Rest Of The Year