Image Source: Zacks Investment ResearchBut is the selling overdone? Let’s take a closer look at how each company stacks up.Tesla Shares Down Almost 30%Down nearly 30% in 2024, Tesla shares have faced a bumpy road, with lower margins and hybrid momentum negatively affecting performance. Analysts have noted the headwinds, lowering their earnings expectations across the board.

Image Source: Zacks Investment ResearchBut is the selling overdone? Let’s take a closer look at how each company stacks up.Tesla Shares Down Almost 30%Down nearly 30% in 2024, Tesla shares have faced a bumpy road, with lower margins and hybrid momentum negatively affecting performance. Analysts have noted the headwinds, lowering their earnings expectations across the board. Image Source: Zacks Investment ResearchStill, shares saw a pop post-earnings following its latest release despite Tesla posting numbers that came in below consensus expectations. Concerning key metrics, TSLA produced over 433,000 vehicles and delivered approximately 387,000 throughout the period.Below is a chart illustrating the company’s gross margin on a trailing twelve-month basis.

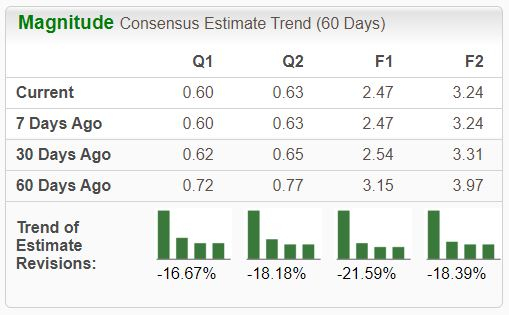

Image Source: Zacks Investment ResearchStill, shares saw a pop post-earnings following its latest release despite Tesla posting numbers that came in below consensus expectations. Concerning key metrics, TSLA produced over 433,000 vehicles and delivered approximately 387,000 throughout the period.Below is a chart illustrating the company’s gross margin on a trailing twelve-month basis. Image Source: Zacks Investment ResearchThe company’s unfavorable earnings outlook will likely continue weighing on share performance, but it continues to focus on cost-cutting exercises to increase operational efficiency. In addition, it’s worth noting that TSLA is part of the AI theme, spending $1 billion on AI infrastructure CapEx throughout its latest period to support autonomous driving efforts.Intel Earnings Forecast Flat YOYLike TSLA, Intel has also suffered negative earnings estimate revisions, with the stock presently carrying a Zacks Rank #4 (Sell). Soft margin and revenue expectations announced for its current period spooked investors, causing shares to see post-earnings pressure following its latest release.

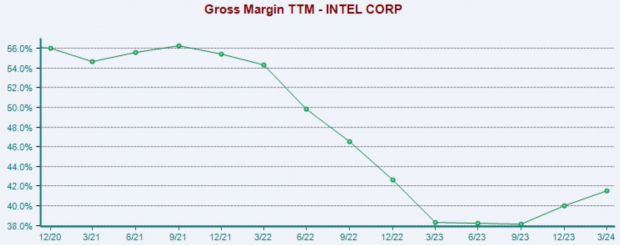

Image Source: Zacks Investment ResearchThe company’s unfavorable earnings outlook will likely continue weighing on share performance, but it continues to focus on cost-cutting exercises to increase operational efficiency. In addition, it’s worth noting that TSLA is part of the AI theme, spending $1 billion on AI infrastructure CapEx throughout its latest period to support autonomous driving efforts.Intel Earnings Forecast Flat YOYLike TSLA, Intel has also suffered negative earnings estimate revisions, with the stock presently carrying a Zacks Rank #4 (Sell). Soft margin and revenue expectations announced for its current period spooked investors, causing shares to see post-earnings pressure following its latest release. Image Source: Zacks Investment ResearchThe company has faced operational issues for some time, with the stock not participating in the AI trade. It’s reasonable to expect shares to continue trading unfavorably until positive earnings estimate revisions begin rolling in, which would likely be sparked by a robust set of quarterly results.Below is a chart illustrating the company’s revenue on an annual basis. Please note that the last value is on a trailing twelve-month basis.

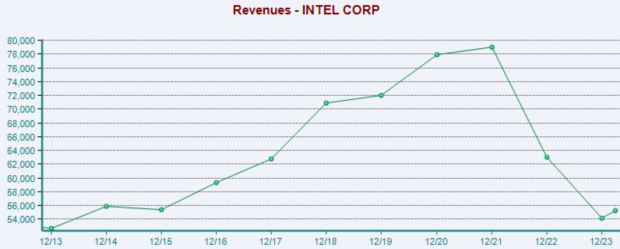

Image Source: Zacks Investment ResearchThe company has faced operational issues for some time, with the stock not participating in the AI trade. It’s reasonable to expect shares to continue trading unfavorably until positive earnings estimate revisions begin rolling in, which would likely be sparked by a robust set of quarterly results.Below is a chart illustrating the company’s revenue on an annual basis. Please note that the last value is on a trailing twelve-month basis. Image Source: Zacks Investment ResearchThe valuation picture for Intel also seems a bit rich, with shares trading at a 28.7X forward earnings multiple (F1). The company’s earnings are forecasted to be flat year-over-year on +2.7% revenue growth, with the stock also carrying a Style Score of ‘F; for Value.Starbucks Facing Pressure in ChinaSlowing business in China has remained a thorn in the company’s side, with China comparable store sales falling 11% on an 8% decline in average ticket in its latest period. North American and U.S. comparable store sales also showed weakness, 3% lower, but did see a 4% increase in average ticket.Concerning headline figures in the print, SBUX fell short of the Zacks Consensus EPS estimate by 14% and posted sales 6.3% below expectations. Both items were down from the year-ago period, with sales of $8.5 billion down 2%.The company’s current earnings outlook reflects the headwinds, with the stock presently carrying a Zacks Rank #4 (Sell).

Image Source: Zacks Investment ResearchThe valuation picture for Intel also seems a bit rich, with shares trading at a 28.7X forward earnings multiple (F1). The company’s earnings are forecasted to be flat year-over-year on +2.7% revenue growth, with the stock also carrying a Style Score of ‘F; for Value.Starbucks Facing Pressure in ChinaSlowing business in China has remained a thorn in the company’s side, with China comparable store sales falling 11% on an 8% decline in average ticket in its latest period. North American and U.S. comparable store sales also showed weakness, 3% lower, but did see a 4% increase in average ticket.Concerning headline figures in the print, SBUX fell short of the Zacks Consensus EPS estimate by 14% and posted sales 6.3% below expectations. Both items were down from the year-ago period, with sales of $8.5 billion down 2%.The company’s current earnings outlook reflects the headwinds, with the stock presently carrying a Zacks Rank #4 (Sell). Image Source: Zacks Investment ResearchNonetheless, the company remains confident, with the CFO stating, “While it was a difficult quarter, we learned from our own underperformance and sharpened our focus with a comprehensive roadmap of well thought out actions making the path forward clear.”Bottom LineWhile many stocks have enjoyed positivity in 2024, not all have seen the same, including Tesla, Starbucks, and Intel.All three have underperformed notably year-to-date, with each also carrying a negative earnings picture. Shares of each will likely continue to face near-term pressure until positive earnings estimate revisions begin rolling in, which would reflect a notable change in sentiment.More By This Author:Dividend Watch: Three Companies Boosting PayoutsBear Of The Day: Cracker Barrel Old Country Store Should You Buy Stock Splits?

Image Source: Zacks Investment ResearchNonetheless, the company remains confident, with the CFO stating, “While it was a difficult quarter, we learned from our own underperformance and sharpened our focus with a comprehensive roadmap of well thought out actions making the path forward clear.”Bottom LineWhile many stocks have enjoyed positivity in 2024, not all have seen the same, including Tesla, Starbucks, and Intel.All three have underperformed notably year-to-date, with each also carrying a negative earnings picture. Shares of each will likely continue to face near-term pressure until positive earnings estimate revisions begin rolling in, which would reflect a notable change in sentiment.More By This Author:Dividend Watch: Three Companies Boosting PayoutsBear Of The Day: Cracker Barrel Old Country Store Should You Buy Stock Splits?