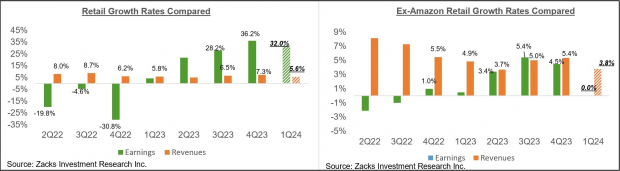

Image Source: Zacks Investment ResearchAs you can see here, these companies have been finding it hard to beat estimates.With respect to earnings and revenue growth rates, we like to show the group’s performance with and without Amazon, whose results are among the 28 companies that have already reported. As we know, Amazon’s Q1 earnings were up +278.7% on +12.5% higher revenues, beating top- and bottom-line expectations.As we all know, digital and brick-and-mortar operators have been converging for some time now, with Amazon now a decent-sized brick-and-mortar operator after Whole Foods and Walmart a growing online vendor. This long-standing trend got a huge boost from the Covid lockdowns.The two comparison charts below show the Q1 earnings and revenue growth relative to other recent periods, both with Amazon’s results (left side chart) and without Amazon’s numbers (right side chart)

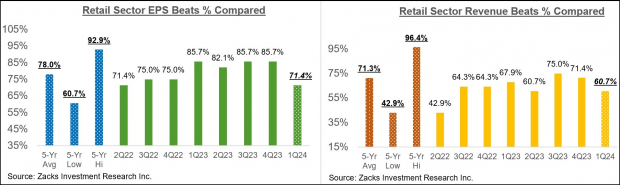

Image Source: Zacks Investment ResearchAs you can see here, these companies have been finding it hard to beat estimates.With respect to earnings and revenue growth rates, we like to show the group’s performance with and without Amazon, whose results are among the 28 companies that have already reported. As we know, Amazon’s Q1 earnings were up +278.7% on +12.5% higher revenues, beating top- and bottom-line expectations.As we all know, digital and brick-and-mortar operators have been converging for some time now, with Amazon now a decent-sized brick-and-mortar operator after Whole Foods and Walmart a growing online vendor. This long-standing trend got a huge boost from the Covid lockdowns.The two comparison charts below show the Q1 earnings and revenue growth relative to other recent periods, both with Amazon’s results (left side chart) and without Amazon’s numbers (right side chart) Image Source: Zacks Investment ResearchAs noted earlier, we have started seeing signs of stress at the lower end of the income distribution. One can intuitively project moderation in consumer spending as the economy further slows down under tighter monetary conditions. Inflation may be down from the multi-decade highs of a few quarters back, but it still remains a headwind, particularly for the lower end of the income distribution. That said, the labor market remains very strong, with wages still going up.Earnings Season Scorecard and This Week’s Earnings ReportsThe bulk of the Q1 earnings season is now behind us, with results from 481 S&P 500 companies already out through Friday, May 24th. We have almost 100 companies reporting results this week, including 10 S&P 500 members. This week’s line-up includes more retailers like Best Buy, Ulta, Dollar General, and Tech players like Salesforce, HP, and others.Total Q1 earnings for these 81 index members are up +7% from the same period last year on +4.4% higher revenues, with 78.2% beating EPS estimates and 60.7% beating revenue estimates.The comparison charts below put the Q1 earnings and revenue growth rates in a historical context.

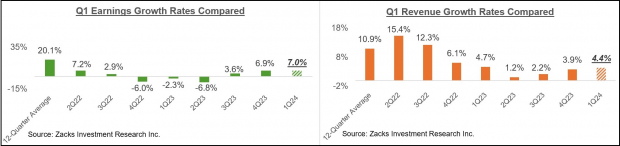

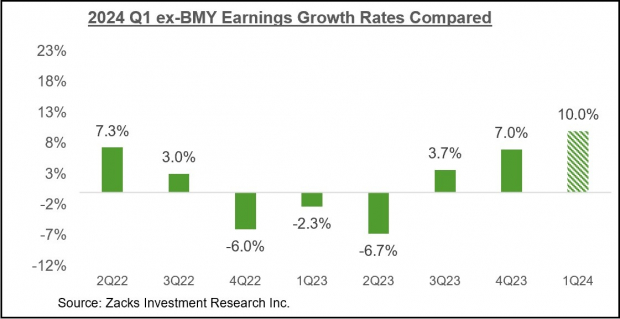

Image Source: Zacks Investment ResearchAs noted earlier, we have started seeing signs of stress at the lower end of the income distribution. One can intuitively project moderation in consumer spending as the economy further slows down under tighter monetary conditions. Inflation may be down from the multi-decade highs of a few quarters back, but it still remains a headwind, particularly for the lower end of the income distribution. That said, the labor market remains very strong, with wages still going up.Earnings Season Scorecard and This Week’s Earnings ReportsThe bulk of the Q1 earnings season is now behind us, with results from 481 S&P 500 companies already out through Friday, May 24th. We have almost 100 companies reporting results this week, including 10 S&P 500 members. This week’s line-up includes more retailers like Best Buy, Ulta, Dollar General, and Tech players like Salesforce, HP, and others.Total Q1 earnings for these 81 index members are up +7% from the same period last year on +4.4% higher revenues, with 78.2% beating EPS estimates and 60.7% beating revenue estimates.The comparison charts below put the Q1 earnings and revenue growth rates in a historical context. Image Source: Zacks Investment ResearchWe have been flagging an acceleration in the earnings growth trend, which becomes more apparent once the Bristol Myers drag is removed from the data; the pharma giant came out with a huge one-time charge. The chart below shows the Q1 earnings growth pace for these companies on an ex-BMY basis.

Image Source: Zacks Investment ResearchWe have been flagging an acceleration in the earnings growth trend, which becomes more apparent once the Bristol Myers drag is removed from the data; the pharma giant came out with a huge one-time charge. The chart below shows the Q1 earnings growth pace for these companies on an ex-BMY basis. Image Source: Zacks Investment ResearchEarnings growth for these companies would have been +10% instead of +7% had it not been for the substantial Energy sector drag.The comparison charts below put the Q1 EPS and revenue beats percentages in a historical context.

Image Source: Zacks Investment ResearchEarnings growth for these companies would have been +10% instead of +7% had it not been for the substantial Energy sector drag.The comparison charts below put the Q1 EPS and revenue beats percentages in a historical context. Image Source: Zacks Investment ResearchAs we noted in the context of the Retail sector, beats percentages have been on the weaker side for the index as a whole, with the variance relative to other recent periods particularly notable on the revenues side.The Earnings Big PictureLooking at Q1 as a whole, total S&P 500 earnings are expected to be up +6.8% from the same period last year on +4.3% higher revenues, which would follow the +6.9% earnings growth on +3.9% revenue gains in the preceding period.The chart below shows current earnings and revenue growth expectations for 2024 Q1 in the context of where growth has been over the preceding four quarters and what is currently expected for the following three quarters.

Image Source: Zacks Investment ResearchAs we noted in the context of the Retail sector, beats percentages have been on the weaker side for the index as a whole, with the variance relative to other recent periods particularly notable on the revenues side.The Earnings Big PictureLooking at Q1 as a whole, total S&P 500 earnings are expected to be up +6.8% from the same period last year on +4.3% higher revenues, which would follow the +6.9% earnings growth on +3.9% revenue gains in the preceding period.The chart below shows current earnings and revenue growth expectations for 2024 Q1 in the context of where growth has been over the preceding four quarters and what is currently expected for the following three quarters. Image Source: Zacks Investment ResearchAs you likely know already, the Tech and Energy sectors are having the opposite effects on the aggregate growth picture. Excluding the Tech sector, Q1 earnings for the rest of the index would be down -0.7%, while the growth pace improves to +9.7% on an ex-energy basis.For the current period (2024 Q2), total S&P 500 earnings are currently expected to be up +9% on +4.6% higher revenues.The revisions trend has been very favorable for Q2 estimates, as the chart below shows.

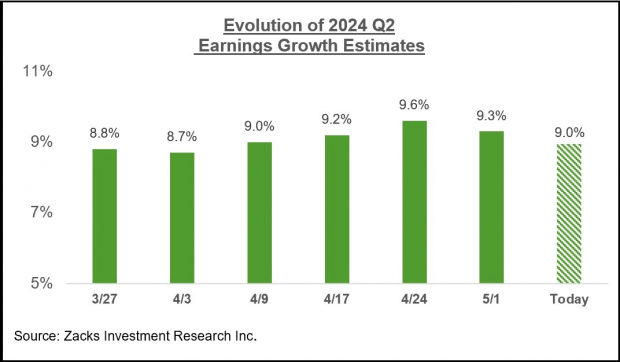

Image Source: Zacks Investment ResearchAs you likely know already, the Tech and Energy sectors are having the opposite effects on the aggregate growth picture. Excluding the Tech sector, Q1 earnings for the rest of the index would be down -0.7%, while the growth pace improves to +9.7% on an ex-energy basis.For the current period (2024 Q2), total S&P 500 earnings are currently expected to be up +9% on +4.6% higher revenues.The revisions trend has been very favorable for Q2 estimates, as the chart below shows. Image Source: Zacks Investment ResearchHere is the Q2 revisions trend on an ex-Energy basis.

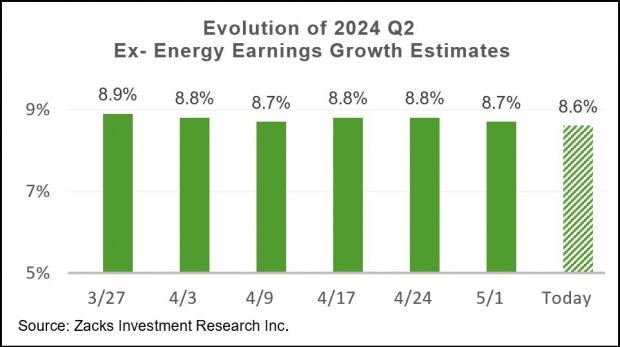

Image Source: Zacks Investment ResearchHere is the Q2 revisions trend on an ex-Energy basis. Image Source: Zacks Investment ResearchLooking at the overall earnings picture on an annual basis, total 2024 S&P 500 earnings are expected to be up +9% on +1.6% revenue growth.

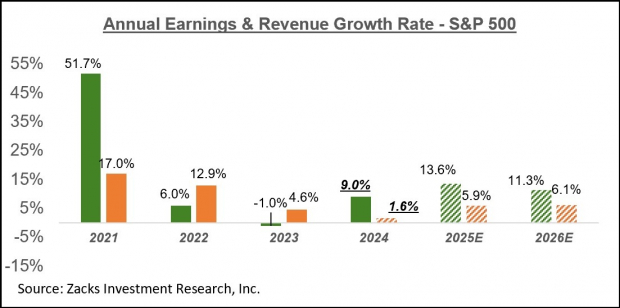

Image Source: Zacks Investment ResearchLooking at the overall earnings picture on an annual basis, total 2024 S&P 500 earnings are expected to be up +9% on +1.6% revenue growth. Image Source: Zacks Investment ResearchMore By This Author:Where Is Earnings Growth Coming From?

Image Source: Zacks Investment ResearchMore By This Author:Where Is Earnings Growth Coming From?

Retail Earnings: A Closer Look

Walmart Earnings And The State Of The Consumer