The Nasdaq and the S&P 500 fell again on Thursday, driven lower by huge pullbacks across software stocks, spurred by Salesforce’s 20% selloff.The market needed a cooldown and Wall Street decided it was time to take profits ahead of the release of the Fed’s preferred inflation gauge on Friday morning. The Nasdaq and the S&P 500 are still riding high heading into June.There could be more near-term profit-taking with plenty of large cap stocks are up well over 30% YTD. Investors should start focusing on taking advantage of any moves down to key moving averages such as the 21-day or 50-day. Wall Street is also likely starting to look for deals as investors take some AI-focused winnings off the table and look to put money to work in beaten-down areas that offer near-term and long-term upside.Today’s episode of Full Court Finance digs into a few reasons behind the recent market dip to close out May. We then explore three oversold S&P 500 stocks—McDonald’s (MCD) , Dollar Tree, Inc. (DLTR) , and Lamb Weston (LW) —that are down at least 15% in 2024 that investors might want to buy right now. Dollar Tree, Inc. The ultra-discount retailer has been hit hard as inflation-squeezed lower-income consumers pull back on spending. Dollar Tree said earlier this year that it would close around 600 unprofitable Family Dollar stores in the first half of FY24 and close 370 Family Dollar and 30 Dollar Tree stores over the next several years at the end of each store’s current lease term. Image Source: Zacks Investment ResearchDLTR is also being hit by theft, lower SNAP benefits, higher gas spending, student-debt repayments restarting, and other headwinds. Dollar Tree stock is down 20% YTD and trading 35% below its peaks because of the changing consumer environment’s impact on its earnings outlook.Dollar Tree has already been punished for its downward EPS revisions, which appear to be leveling off recently. DLTR is still expected to grow its adjusted earnings by 17% in FY24 and 18% next year on 2.5% and 6%, respective revenue expansion.

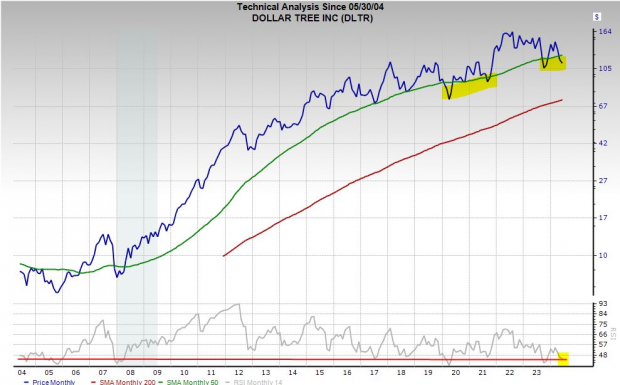

Image Source: Zacks Investment ResearchDLTR is also being hit by theft, lower SNAP benefits, higher gas spending, student-debt repayments restarting, and other headwinds. Dollar Tree stock is down 20% YTD and trading 35% below its peaks because of the changing consumer environment’s impact on its earnings outlook.Dollar Tree has already been punished for its downward EPS revisions, which appear to be leveling off recently. DLTR is still expected to grow its adjusted earnings by 17% in FY24 and 18% next year on 2.5% and 6%, respective revenue expansion. Image Source: Zacks Investment ResearchDollar Tree shares have soared 1,100% in the past 20 years to blow away Walmart’s (WMT) 250% and Dollar General’s (DG) 450%. DLTR appears to be finding support near its 50-month moving average—a level it hasn’t traded below for long over the past two decades.DLTR is sitting at historically oversold RSI levels. Valuation wise, Dollar Tree is trading 34% below its highs and 15% below its median at 15.6X forward earnings.Dollar Tree reports its first quarter results on Wednesday, June 5. McDonald’sThe burger giant, like Dollar Tree, is getting stung by slowing spending from lower-income consumers. McDonald’s also said in its Q1 release that the “continued impact of the war in the Middle East more than offset positive comparable sales in Japan, Latin America and Europe.” McDonald’s is now laser focused on rolling out deals to attract consumers this summer.

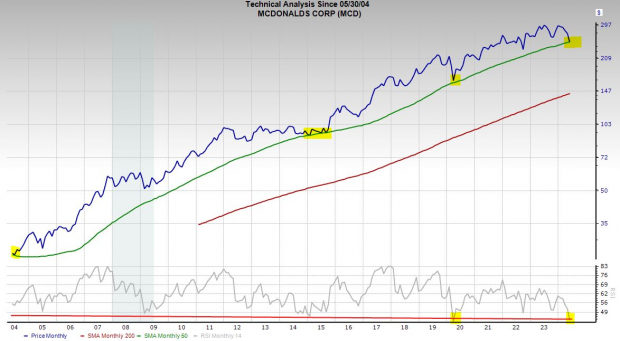

Image Source: Zacks Investment ResearchDollar Tree shares have soared 1,100% in the past 20 years to blow away Walmart’s (WMT) 250% and Dollar General’s (DG) 450%. DLTR appears to be finding support near its 50-month moving average—a level it hasn’t traded below for long over the past two decades.DLTR is sitting at historically oversold RSI levels. Valuation wise, Dollar Tree is trading 34% below its highs and 15% below its median at 15.6X forward earnings.Dollar Tree reports its first quarter results on Wednesday, June 5. McDonald’sThe burger giant, like Dollar Tree, is getting stung by slowing spending from lower-income consumers. McDonald’s also said in its Q1 release that the “continued impact of the war in the Middle East more than offset positive comparable sales in Japan, Latin America and Europe.” McDonald’s is now laser focused on rolling out deals to attract consumers this summer. Image Source: Zacks Investment ResearchMcDonald’s is still projected to grow its global comparable sales by 2.3% in 2024. This marks a slowdown from three straight years of booming comps expansion, including a 9% surge last year.MCD is projected to grow its revenue by over 4% in 2024 and 6% next year to boost adjusted earnings by 2% and 8%, respectively. This bottom-line growth follows 18% adjusted EPS expansion last year. Despite its recent downward EPS revision, MCD’s consensus estimates for 2024 and 2025 remain above where they were this time last year.

Image Source: Zacks Investment ResearchMcDonald’s is still projected to grow its global comparable sales by 2.3% in 2024. This marks a slowdown from three straight years of booming comps expansion, including a 9% surge last year.MCD is projected to grow its revenue by over 4% in 2024 and 6% next year to boost adjusted earnings by 2% and 8%, respectively. This bottom-line growth follows 18% adjusted EPS expansion last year. Despite its recent downward EPS revision, MCD’s consensus estimates for 2024 and 2025 remain above where they were this time last year. Image Source: Zacks Investment ResearchMcDonald’s has slipped 15% YTD and it trades 27% below its average Zacks price target. The fast-food powerhouse appears to be finding support at its 50-month moving average, a level it hasn’t fallen below during the last 20 years.MCD is historically oversold and trading at its lowest forward earnings multiple during the last five years outside of the Covid selloff. McDonald’s is also an S&P 500 Dividend Aristocrat that’s yielding 2.7% right now. Lamb Weston Holdings, Inc.Lamb Weston’s frozen potatoes business is boring but booming. Yet the stock has tanked 21% YTD after it missed our Q3 2024 EPS estimates and slashed its guidance as it faces setbacks amid its transitions to a new planning system.“The enterprise resource planning (ERP) transition temporarily reduced the visibility of finished goods inventories located at distribution centers, which affected our ability to fill customer orders… While we are disappointed with the magnitude of the ERP transition’s effect on the quarter,” CEO Tom Werner said in its quarterly release.

Image Source: Zacks Investment ResearchMcDonald’s has slipped 15% YTD and it trades 27% below its average Zacks price target. The fast-food powerhouse appears to be finding support at its 50-month moving average, a level it hasn’t fallen below during the last 20 years.MCD is historically oversold and trading at its lowest forward earnings multiple during the last five years outside of the Covid selloff. McDonald’s is also an S&P 500 Dividend Aristocrat that’s yielding 2.7% right now. Lamb Weston Holdings, Inc.Lamb Weston’s frozen potatoes business is boring but booming. Yet the stock has tanked 21% YTD after it missed our Q3 2024 EPS estimates and slashed its guidance as it faces setbacks amid its transitions to a new planning system.“The enterprise resource planning (ERP) transition temporarily reduced the visibility of finished goods inventories located at distribution centers, which affected our ability to fill customer orders… While we are disappointed with the magnitude of the ERP transition’s effect on the quarter,” CEO Tom Werner said in its quarterly release. Image Source: Zacks Investment ResearchLamb Weston believes the impact is in the rearview as its “order fulfillment rates have normalized.” The company’s earnings outlook has fallen recently, but its outlook for FY24 and FY25 remain solidly above where they were this time last year. LW is projected to grow its sales by 23% in its FY24 and add another 3% next year to boost its bottom line by 18% and 12%, respectively.

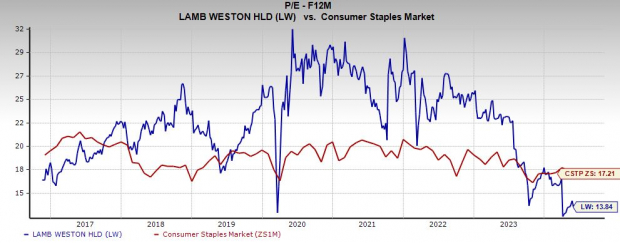

Image Source: Zacks Investment ResearchLamb Weston believes the impact is in the rearview as its “order fulfillment rates have normalized.” The company’s earnings outlook has fallen recently, but its outlook for FY24 and FY25 remain solidly above where they were this time last year. LW is projected to grow its sales by 23% in its FY24 and add another 3% next year to boost its bottom line by 18% and 12%, respectively.  Image Source: Zacks Investment ResearchThe Lamb Weston is down 21% YTD and trades 31% below its average Zacks price target. LW is still up 45% in the last five years to blow away the Zacks Consumer Staples sector’s sideways run.LW found support at its 200-week moving average. Plus it trades at a 56% discount to its highs and near its all-time Covid lows at 13.8X forward earnings. Lamb Weston also pays a dividend that yields 1.7%. More By This Author:Bear Of The Day: O-I Glass, Inc. Buy This Surging Tech Stock Now and Hold?2 Great Stocks to Buy Now at Huge Discounts Heading into June

Image Source: Zacks Investment ResearchThe Lamb Weston is down 21% YTD and trades 31% below its average Zacks price target. LW is still up 45% in the last five years to blow away the Zacks Consumer Staples sector’s sideways run.LW found support at its 200-week moving average. Plus it trades at a 56% discount to its highs and near its all-time Covid lows at 13.8X forward earnings. Lamb Weston also pays a dividend that yields 1.7%. More By This Author:Bear Of The Day: O-I Glass, Inc. Buy This Surging Tech Stock Now and Hold?2 Great Stocks to Buy Now at Huge Discounts Heading into June