A ‘wall of money’ coming at the market is a common refrain this year; but is it really what’s happening? Nope … essentially it’s been like a sole concentrated entry point (a border crossing ignoring a dozen nearby) that becomes jammed, or a ‘bottleneck’, in a sense, as the rush of buyers into just a handful, levitates those stocks and generally not others.There’s of course the example of Nvidia; but there’s also panting gambling as seen you in GameStop, which soared and then totally got floored (remember I speculated that ‘Savvy Kitty’ was feeding shares into the rally he triggered … making it a sell not buy). So for me I prefer looking at what might be next as opposed to what already transpired (and hence has more latecomer risk).

Market X-ray: Nothing of priority or dramatic is happening; as we all await Apple WWDC. With that said; the Nvidia split is effective as of now; and we’ll see if oddly the revelations this coming week from Apple sort of keep the sector energy alive. My interpretations of the Jobs data could allow for the friendlier Fed ahead. It’s implying a weaker economy with many people struggling to make ends meet.

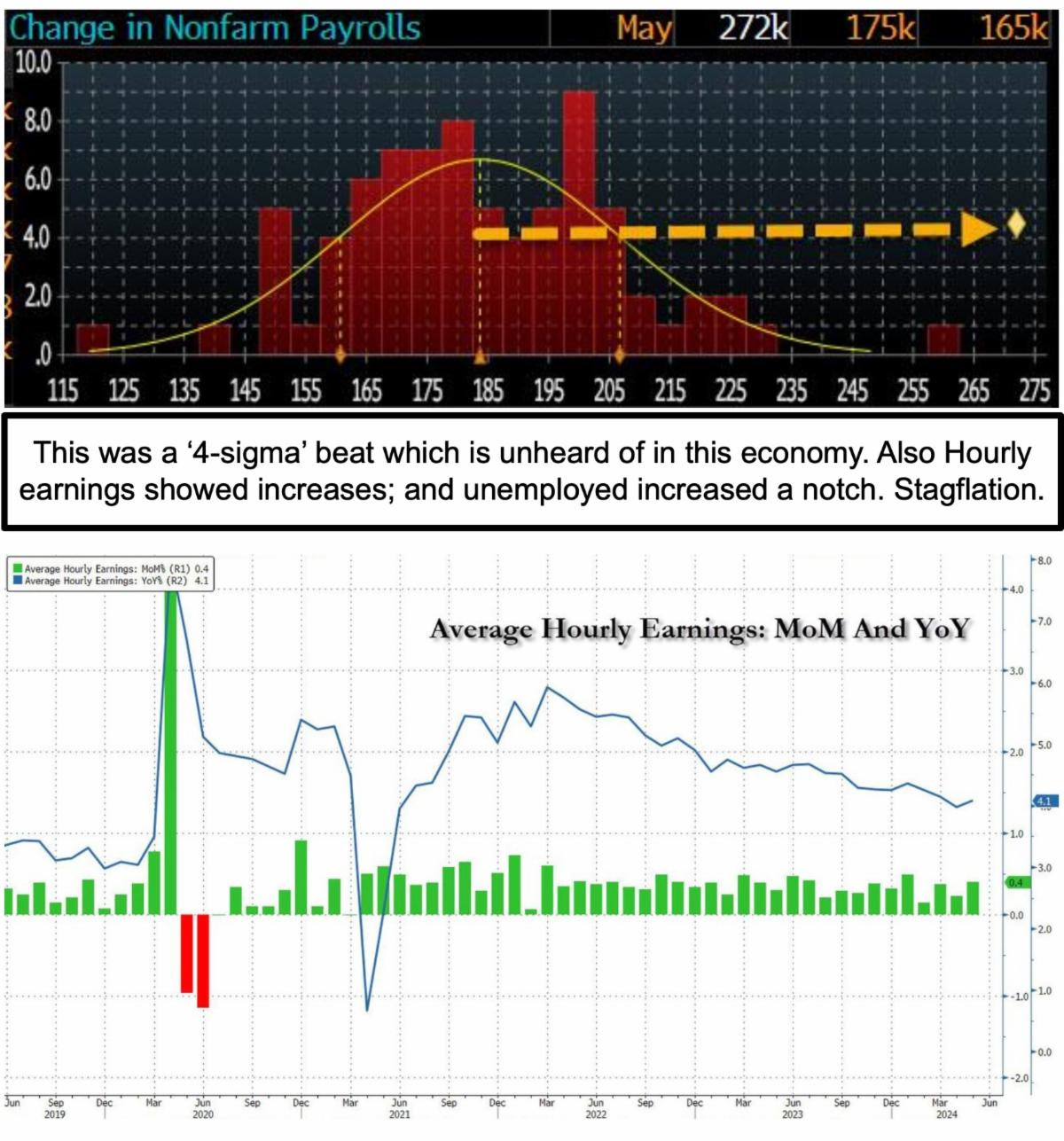

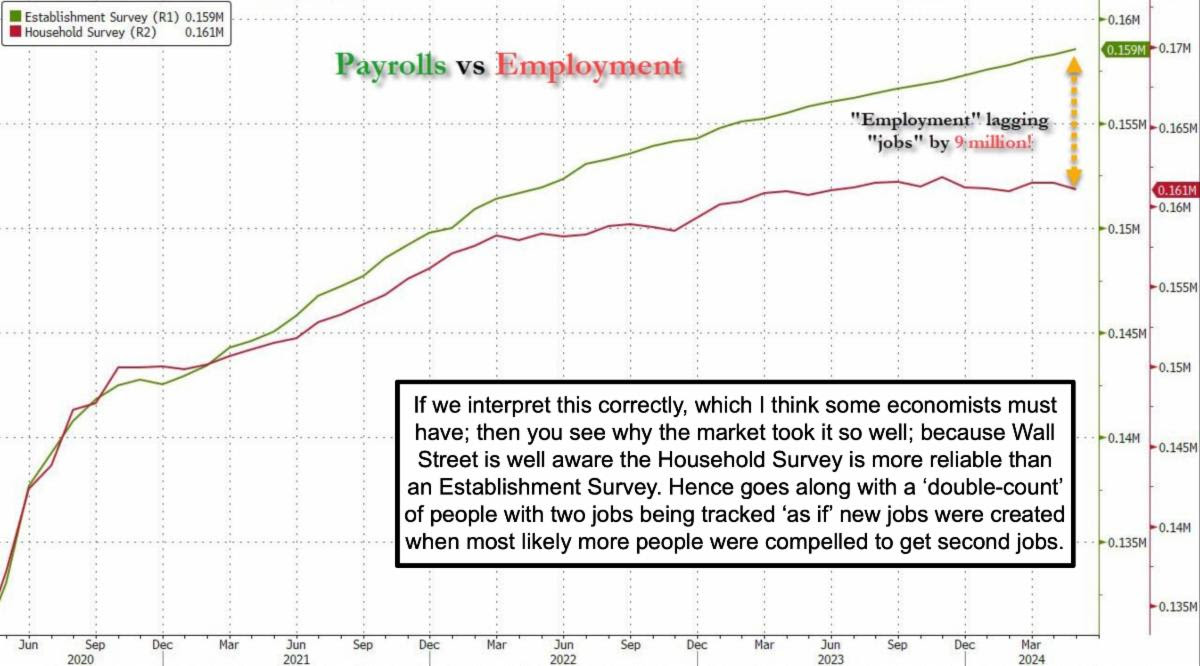

Market X-ray: Nothing of priority or dramatic is happening; as we all await Apple WWDC. With that said; the Nvidia split is effective as of now; and we’ll see if oddly the revelations this coming week from Apple sort of keep the sector energy alive. My interpretations of the Jobs data could allow for the friendlier Fed ahead. It’s implying a weaker economy with many people struggling to make ends meet. I should mention that the market’s ability to generally absorb higher NFP data (Non-Farm Payroll) on Friday is a plus; even as hedges and Indexes lost just a bit of luster. The point is that S&P didn’t ‘tank’, and that’s a plus for those of managers anticipating further upside, especially as we head towards July. If you looked at the charts above, you know why I question the Friday reports.It’s a phony number of course; since it was ‘jobs’ not ‘workers’ being counted. A lot of people must work two jobs to survive; so you get ‘double-counting’ as well as the reason the so-called ‘hot’ NFP number exceeded the ADP decline (actually the opposite; but ADP is based on ‘workers’ not need for extra jobs). I doubt any media, and certainly not the White House, will note that key detail.Of course there are many variables to consider; and we’re open-minded for a more meaningful shakeout, but it’s not (barring exogenous events) likely to be anything calamitous (again depends on war(s) and possibly domestic politics, if the roster of candidates was to change on either side for any reason).

I should mention that the market’s ability to generally absorb higher NFP data (Non-Farm Payroll) on Friday is a plus; even as hedges and Indexes lost just a bit of luster. The point is that S&P didn’t ‘tank’, and that’s a plus for those of managers anticipating further upside, especially as we head towards July. If you looked at the charts above, you know why I question the Friday reports.It’s a phony number of course; since it was ‘jobs’ not ‘workers’ being counted. A lot of people must work two jobs to survive; so you get ‘double-counting’ as well as the reason the so-called ‘hot’ NFP number exceeded the ADP decline (actually the opposite; but ADP is based on ‘workers’ not need for extra jobs). I doubt any media, and certainly not the White House, will note that key detail.Of course there are many variables to consider; and we’re open-minded for a more meaningful shakeout, but it’s not (barring exogenous events) likely to be anything calamitous (again depends on war(s) and possibly domestic politics, if the roster of candidates was to change on either side for any reason). Mixed Jobs Report; mixed market reaction. Market consolidating and holding most gains or just lateral behavior in a myriad of stocks. The market didn’t get the permission to celebrate lower yields (but may happen anyway); while this does suggest pockets of strength and earnings power actually matters.This is all tough as the average consumer struggles with inflation and I think it is a ‘bifurcated’ stagflation as contended for months, when sorting it all out. If anything, even the ‘big retailer’ battles (like Walmart, vs. Target even Amazon) are indicative of pressure to be profitable but give a nod of value orientation to consumers (which prices generally do not do). And by the way more things do get made in America (which I’ve always favored), the harder it will be to drop prices, and just the treat of bargain-basement EV autos from China revealed it to this Nation; as Washington rightly wants U.S. content; but can’t have it both ways if they want things made here but insist that prices will falter. Hence part of my consistent argument that prices ‘at best’ can only slow the pace of rise; as citizens / consumers / workers have to adjust to higher overall price levels.

Mixed Jobs Report; mixed market reaction. Market consolidating and holding most gains or just lateral behavior in a myriad of stocks. The market didn’t get the permission to celebrate lower yields (but may happen anyway); while this does suggest pockets of strength and earnings power actually matters.This is all tough as the average consumer struggles with inflation and I think it is a ‘bifurcated’ stagflation as contended for months, when sorting it all out. If anything, even the ‘big retailer’ battles (like Walmart, vs. Target even Amazon) are indicative of pressure to be profitable but give a nod of value orientation to consumers (which prices generally do not do). And by the way more things do get made in America (which I’ve always favored), the harder it will be to drop prices, and just the treat of bargain-basement EV autos from China revealed it to this Nation; as Washington rightly wants U.S. content; but can’t have it both ways if they want things made here but insist that prices will falter. Hence part of my consistent argument that prices ‘at best’ can only slow the pace of rise; as citizens / consumers / workers have to adjust to higher overall price levels. Bottom line: a hot Jobs report initially hit the market, then recovered more or less to a ‘flat’ scenario ahead of the AI revelations from Apple. Again; when a relatively intelligent Fed looks at Non-Farm Payrolls they won’t be impressed, because they know that the BLS ‘double-counted’ anyone with two jobs. In a sense in a ‘truly strong’ economy, you wouldn’t need two jobs just to get by..The ‘meme’ GameStop ‘crash’ illustrates what can happen to stock squeezes ‘without’ much going for them. The market needs defensive stocks and even international stocks to ‘broaden’ a good bit more; as we have not had a broad breadth market; and that’s why it is not only so hard to make money; but also why it’s hard to be bearish with a realization it’s an Election Year and probably interest rates coming lower, as a key driver for stocks as time goes on and investors shying away from recent concentration on Utilities or other interest-rate sensitive areas.Enjoy the weekend, and lets’s see what JG at Apple has to say (came from Google as Tim Cook enticed Giannandrea to run AI over at Apple). Whether he is formally introduced in the Presentation or not, it’s the reported ‘OpenAI’ deal that will be primarily of interest, and whether Microsoft is a beneficiary, or (as I suspect) Apple will structures all this to run best on Apple hardware.Conclusion for now: the market was relieved growth wasn’t slipping more. So that leaves the economy (and even the survey) mixed and confusing. But the productivity growth is acceptable; and reconstruction (hate to call it a ‘boom’) from storms and the coming hurricanes (sorry to say) is something pending. I don’t want to see the latter; but realistically that prospect is looming stronger.

Bottom line: a hot Jobs report initially hit the market, then recovered more or less to a ‘flat’ scenario ahead of the AI revelations from Apple. Again; when a relatively intelligent Fed looks at Non-Farm Payrolls they won’t be impressed, because they know that the BLS ‘double-counted’ anyone with two jobs. In a sense in a ‘truly strong’ economy, you wouldn’t need two jobs just to get by..The ‘meme’ GameStop ‘crash’ illustrates what can happen to stock squeezes ‘without’ much going for them. The market needs defensive stocks and even international stocks to ‘broaden’ a good bit more; as we have not had a broad breadth market; and that’s why it is not only so hard to make money; but also why it’s hard to be bearish with a realization it’s an Election Year and probably interest rates coming lower, as a key driver for stocks as time goes on and investors shying away from recent concentration on Utilities or other interest-rate sensitive areas.Enjoy the weekend, and lets’s see what JG at Apple has to say (came from Google as Tim Cook enticed Giannandrea to run AI over at Apple). Whether he is formally introduced in the Presentation or not, it’s the reported ‘OpenAI’ deal that will be primarily of interest, and whether Microsoft is a beneficiary, or (as I suspect) Apple will structures all this to run best on Apple hardware.Conclusion for now: the market was relieved growth wasn’t slipping more. So that leaves the economy (and even the survey) mixed and confusing. But the productivity growth is acceptable; and reconstruction (hate to call it a ‘boom’) from storms and the coming hurricanes (sorry to say) is something pending. I don’t want to see the latter; but realistically that prospect is looming stronger. More By This Author:Market Briefing For Thursday June 6

More By This Author:Market Briefing For Thursday June 6

Market Briefing For Wednesday June 5

Market Briefing For Monday June 3