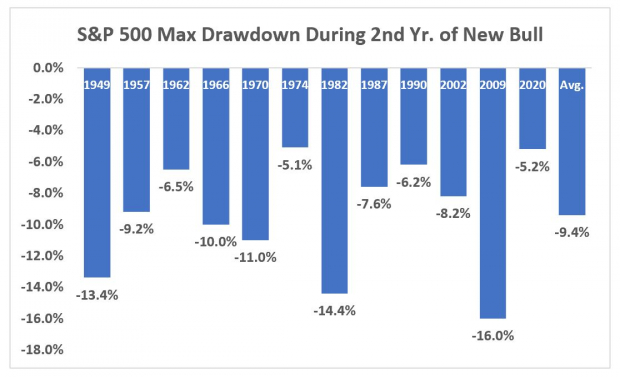

Image: BigstockThis year’s market rally has come with minimal gut-check moments for investors. We remain in the midst of one of them.Even after the recent declines, the S&P 500 was still up better than 13% following Thursday’s close. The largest drawdown we’ve experienced this year has been about 6%, which came back in the spring during the normally bullish month of April.As we can see below, the average drawdown during the second year of a new bull market is 9.4% (note that the years show when new bulls begin):

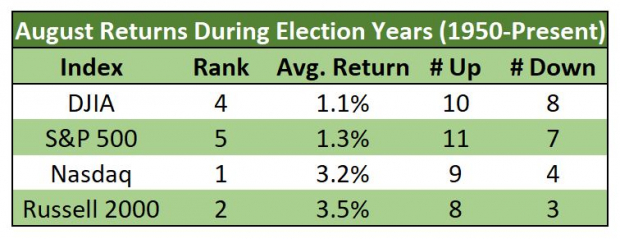

Image: BigstockThis year’s market rally has come with minimal gut-check moments for investors. We remain in the midst of one of them.Even after the recent declines, the S&P 500 was still up better than 13% following Thursday’s close. The largest drawdown we’ve experienced this year has been about 6%, which came back in the spring during the normally bullish month of April.As we can see below, the average drawdown during the second year of a new bull market is 9.4% (note that the years show when new bulls begin): Image Source: Zacks Investment ResearchWhile seasonality dictates that a sharper pullback is more likely to arrive in the September-October timeframe, we know that anything is possible in the stock market. Making drastic changes to portfolio allocations based on short-term price movements is a recipe for disaster.Keeping seasonals in mind, this current market volatility may be paving the way for an uptick heading into August. Of course, we need to eliminate feelings or emotions when it comes to investing. We rely on facts; seasonal statistics point to a heightened probability of strength next month.The month of August tends to hold up well in election years, and this recent weakness may just be some overdue selling pressure amid early earnings season jitters. In fact, dating back to 1950, the month of August ranks first out of all 12 months for the Nasdaq during election years, with an average return of 3.2%:

Image Source: Zacks Investment ResearchWhile seasonality dictates that a sharper pullback is more likely to arrive in the September-October timeframe, we know that anything is possible in the stock market. Making drastic changes to portfolio allocations based on short-term price movements is a recipe for disaster.Keeping seasonals in mind, this current market volatility may be paving the way for an uptick heading into August. Of course, we need to eliminate feelings or emotions when it comes to investing. We rely on facts; seasonal statistics point to a heightened probability of strength next month.The month of August tends to hold up well in election years, and this recent weakness may just be some overdue selling pressure amid early earnings season jitters. In fact, dating back to 1950, the month of August ranks first out of all 12 months for the Nasdaq during election years, with an average return of 3.2%: Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Key Inflation Measure Continues to Subside

U.S. stocks snapped back in early trading on Friday, poised to regain key levels as investors embraced new data that reinforced the easing inflation trend.The Personal Consumption Expenditures (PCE) index from June rose 2.5% year-over-year, matching economists’ projections. The index climbed 0.1% on the month, also in line with estimates.The “core” PCE, which is the Fed’s preferred inflation gauge and strips out the costs of food and energy, rose 2.6% over the prior year. While the figure came in slightly above the median estimate of 2.5%, the print still marked the slowest annual increase in more than three years. The ongoing disinflation adds credence to the notion of upcoming interest rate cuts.The Fed’s next monetary policy decision will come next week on July 31. Market participants are currently pricing in just a 5% chance of a cut next week. However, odds of a rate cut have jumped to 100% at the September meeting.

Second-Quarter Earnings Season Heats Up

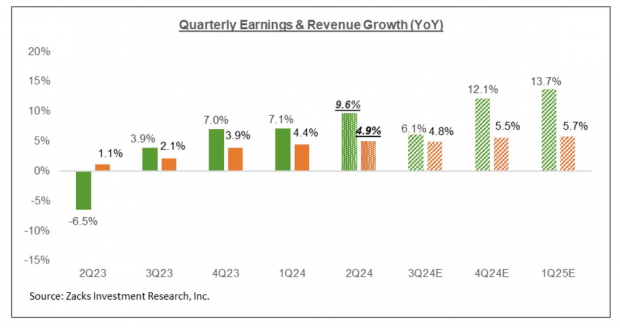

The Q2 earnings picture is now in full swing. We know that markets rallied sharply into the season, so it’s not all that surprising to encounter some volatility as the numbers roll in.The S&P 500 is down about 4% since July 16, so it looks like we’re seeing that play out now. As we noted, this selling bout could be paving the way for seasonal strength into August.Second-quarter earnings results have been solid. Through Wednesday’s close, 134 S&P 500 companies reported Q2 results, or about 26.8% of the index’s membership. Total earnings are up 7.6% from the same period last year on 4.7% higher revenues.Overall, total Q2 earnings are expected to be up 9.6% from the year-ago period on 4.9% higher revenues. This would be the best earnings growth pace since the 10% year-over-year improvement witnessed in Q1 of 2022. Image Source: Zacks Investment ResearchNext week is a very busy one in terms of earnings, particularly on the tech front with four of the “Magnificent 7” members reporting results. Microsoft (MSFT – Free Report) will deliver its numbers on Tuesday, Facebook-parent Meta Platforms (META – Free Report) will post on Wednesday, followed by Apple (AAPL – Free Report), and Amazon (AMZN – Free Report) on Thursday.

Image Source: Zacks Investment ResearchNext week is a very busy one in terms of earnings, particularly on the tech front with four of the “Magnificent 7” members reporting results. Microsoft (MSFT – Free Report) will deliver its numbers on Tuesday, Facebook-parent Meta Platforms (META – Free Report) will post on Wednesday, followed by Apple (AAPL – Free Report), and Amazon (AMZN – Free Report) on Thursday.

Final Thoughts

A continued bright spot has been small-caps; the Russell 2000’s outperformance has picked up in recent sessions. The longer the move persists, the more relevant it becomes.Market breadth has also held up better than we’d expect during this most recent pullback. In fact, back on Wednesday’s drubbing, when the S&P 500 fell more than 2%, one-third of stocks within the index actually rose. It was the best breadth on a 2% down day dating back to October 2000.Notably, the volatility (VIX) index is reversing from a three-month high. It’s been a “buy the dip” market this year, so adding exposure during the rare spikes in volatility has been the way to go. We’ll see if stocks can turn the corner as we head deeper into the Q2 earnings season.More By This Author:3 Iconic Companies To Buy Stock In After EarningsBull Of The Day: The Progressive Bear of the Day: Kohls