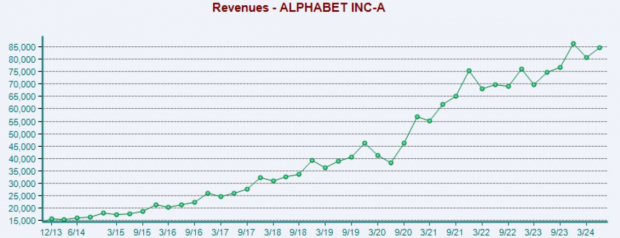

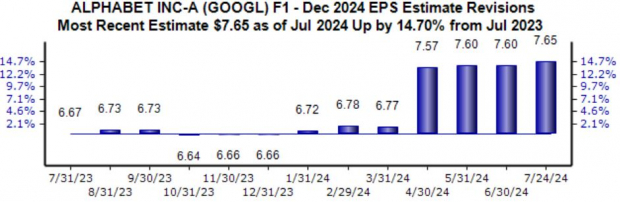

Mega-cap technology giant Alphabet (GOOGL) recently reported quarterly results, helping kick off the reporting cycle for the Mag 7 group. So far, we’ve also heard from Tesla, with the rest of the group’s results expected in the coming weeks.The reaction to Alphabet’s quarterly release was initially negative, raising the eyebrows of some and halting recent momentum. The results provide some read-through for Meta Platforms’ (META) upcoming release, particularly concerning advertising results.Let’s take a closer look at the results. Alphabet Posts Record Cloud RevenueAlphabet’s quarterly release was overall positive, with the company enjoying 31% EPS growth on nearly 14% higher sales. Both figures exceeded our consensus expectations, building on its recent streak of quarterly positivity.Advertising revenue reached $64.6 billion, showing a 12% climb relative to the year-ago figure. Cloud also showed great growth, with revenues of $10.3 billion nearly 30% higher year-over-year and reflecting a quarterly record.Below is a chart illustrating the company’s total revenue on a quarterly basis. Image Source: Zacks Investment ResearchThe knee-jerk reaction following the print was likely a reflection of profit-taking after a strong run, with the CEO’s comments concerning artificial intelligence (AI) CapEx spooking some. CapEx throughout the period totaled $13.2 billion, higher than expected due to investments in servers and data centers.When asked about CapEx levels, CEO Sundar Pichai said, ‘The one way I think about it is when you go through a curve like this, the risk of underinvesting is dramatically greater than the risk of overinvesting for us here. Even in scenarios where if it turns out we are overinvesting, these are infrastructure which are widely useful for us, they have long useful lives, and we can apply it across and we can work through that.’Investors will undoubtedly remain curious about the return on AI investment, but the company overall maintains a bright outlook concerning the future benefits. Analysts have kept their earnings expectations for its current fiscal year stable following the release, with the $7.65 per share expected suggesting 32% Y/Y growth.

Image Source: Zacks Investment ResearchThe knee-jerk reaction following the print was likely a reflection of profit-taking after a strong run, with the CEO’s comments concerning artificial intelligence (AI) CapEx spooking some. CapEx throughout the period totaled $13.2 billion, higher than expected due to investments in servers and data centers.When asked about CapEx levels, CEO Sundar Pichai said, ‘The one way I think about it is when you go through a curve like this, the risk of underinvesting is dramatically greater than the risk of overinvesting for us here. Even in scenarios where if it turns out we are overinvesting, these are infrastructure which are widely useful for us, they have long useful lives, and we can apply it across and we can work through that.’Investors will undoubtedly remain curious about the return on AI investment, but the company overall maintains a bright outlook concerning the future benefits. Analysts have kept their earnings expectations for its current fiscal year stable following the release, with the $7.65 per share expected suggesting 32% Y/Y growth.

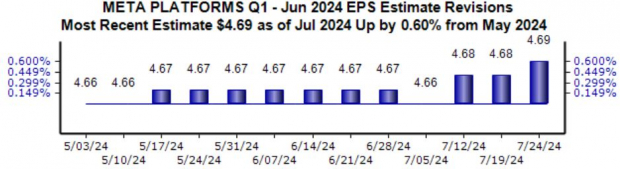

Image Source: Zacks Investment ResearchSo, while shares had a rough initial reaction, the company’s print was overall highly positive, with cloud and advertising showing strong growth. The negativity could likely be attributed to profit-taking and uncertainty surrounding CapEx levels. Meta’s Quarterly Results LoomMETA’s quarterly results are expected on July 31st after the close. The company’s improved operational efficiencies have aided its profitability significantly, with EPS growing 80% throughout its latest quarter.The sell-off following its latest print can be attributed to its announcement of higher CapEx for the current fiscal year, which was raised to a band of $35 – $40 billion (previously $30 – $37 billion). Meta raised its CapEx to accelerate its infrastructure investments for its artificial intelligence (AI) roadmap, also expecting higher CapEx for next year to support its efforts.Investors will undoubtedly be looking for more color on CapEx trends surrounding AI, just like we saw in Alphabet’s quarterly release. Earnings expectations for the release have ticked higher over recent months, with the $4.69 per share expected reflecting 45% Y/Y growth.

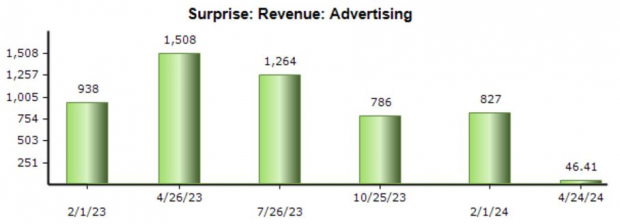

Image Source: Zacks Investment ResearchConcerning key metrics, the Zacks Consensus Estimate for Advertising revenue stands at $37.5 billion, 20% higher than the year-ago period. The company’s Advertising results have consistently beaten our expectations recently, but the beats have gotten increasingly smaller, as shown below.

Image Source: Zacks Investment ResearchIn addition, META shares aren’t expensive heading into the release, with the current 21.2X forward 12-month earnings multiple in line with the five-year median and well beneath five-year highs of 37.0X. The current PEG ratio also works out to 1.1X, reflecting that investors are paying a fair price for the forecasted growth. Bottom LineAlphabet’s quarterly release brought about some selling pressure, with comments surrounding AI CapEx causing some spooks. Meta Platforms experienced the same post-earnings fate following its latest release for the same reason, but shares have since recovered.All in all, it was a solid print from Alphabet, with all aspects of the business performing nicely. The favorable advertising results provide us with a decent read-through of what to expect from Meta Platforms concerning its advertising business, and investors should also expect scrutiny surrounding CapEx.More By This Author:Mag 7 Earnings Loom: A Closer Look

What’s Going On With The Mag 7?

Airliner Earnings: Should You Buy?