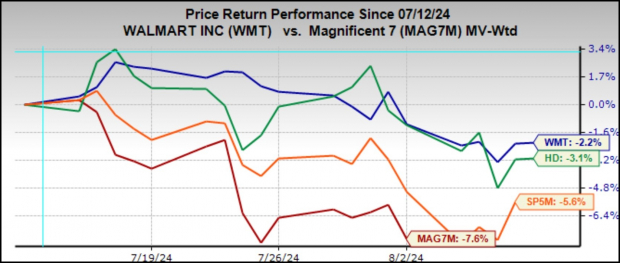

Image Source: Zacks Investment ResearchWalmart’s defensive attributes reflect the retailer’s heavy grocery exposure and reputation for value. Walmart’s value orientation and well-executed digital strategy have been key to gaining grocery market share by attracting higher-income households.Walmart’s growing share of higher-income grocery spending notwithstanding, the retailer still has a substantial exposure to lower-income consumers, who appear to be under growing stress, as reflected in rising loan delinquency rates and other measures indicating strained financial health. This exposure could be a source of vulnerability for Walmart’s same-store sales in its quarterly release.Walmart is expected to report $0.65 in EPS on $168.4 billion in revenues, representing year-over-year changes of +6.6% and +4.2%, respectively. Trends in Walmart’s non-grocery business have been anemic lately, though management had pointed to some early signs of stabilization in a few discretionary product categories at the last earnings call. Any favorable turn in the demand trends for the retailer’s discretionary merchandise will be a nice offset to the aforementioned lower-income vulnerability. Any signs of life on the discretionary merchandise part will also have positive read-throughs for Target (TGT – Free Report).The chart below uses a longer time span than the four-week period we used earlier, with the one-year performance of Walmart relative to Home Depot, Mag 7, and the S&P 500 index.

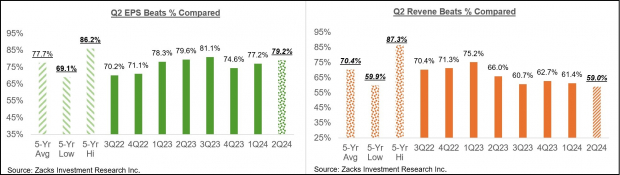

Image Source: Zacks Investment ResearchWalmart shares were up big following the last quarterly release on May 15th, which was the second quarter in a row of market participants cheering the retailer’s quarterly results. One relatively less noted part of Walmart’s growing digital footprint is the retailer’s growing advertising business. It is still a relatively small part of Walmart’s total revenues, but this revenue stream is growing fast and enjoys a much higher margin.With respect to the Retail sector 2024 Q2 earnings season scorecard, we now have results from 23 of the 36 retailers in the S&P 500 index. Regular readers know that Zacks has a dedicated stand-alone economic sector for the retail space, which is unlike the placement of the space in the Consumer Staples and Consumer Discretionary sectors in the Standard & Poor’s standard industry classification.The Zacks Retail sector includes not only Walmart, Home Depot, and other traditional retailers but also online vendors like Amazon (AMZN – Free Report) and restaurant players. The 23 Zacks Retail companies in the S&P 500 index that have reported Q2 results already belong to the e-commerce and restaurant industries.Total Q2 earnings for these 23 retailers that have reported are up +26.2% from the same period last year on +6.1% higher revenues, with 52.2% beating EPS estimates and only 34.8% beating revenue estimates.The comparison charts below put the Q2 beats percentages for these retailers in a historical context.

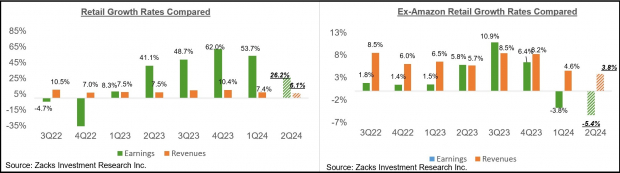

Image Source: Zacks Investment ResearchAs you can see above, the online players and restaurant operators have struggled with beating EPS and revenue estimates in Q2. In fact, Q2 EPS and revenue beats percentages for these players represent a new low over the preceding 20 quarters (5 years).With respect to the elevated earnings rate at this stage, we like to show the group’s performance with and without Amazon, whose results are among the 23 companies that have reported already. As we know, Amazon’s Q2 earnings were up +99.8% on +10.1% higher revenues, as it beat on EPS but missed top- line expectations.As we all know, digital and brick-and-mortar operators have been converging for some time now. Amazon is now a decent-sized brick-and-mortar operator after Whole Foods, and Walmart is a growing online vendor. As we noted in the context of discussing Walmart’s results, the retailer is steadily becoming a big advertising player thanks to its growing digital business. This long-standing trend got a huge boost from the COVID lockdowns.The two comparison charts below show the Q2 earnings and revenue growth relative to other recent periods, both with Amazon’s results (left side chart) and without Amazon’s numbers (right side chart)

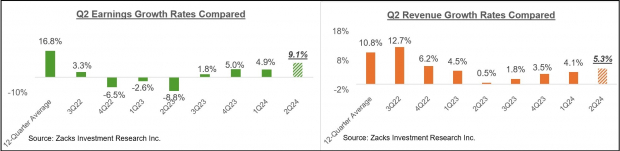

Image Source: Zacks Investment ResearchAs noted earlier, we have started seeing signs of stress at the lower end of income distribution, and one can intuitively project moderation in consumer spending as the economy further slows down under the weight of tighter monetary conditions. Inflation may be down from the multi-decade highs of a few quarters back, but it still remains a headwind, particularly for the lower end of income distribution. That said, the labor market remains very strong, with wages still going up.We will hear more about issues on the Q2 earnings calls, as we did from Amazon, likely in the context of their outlooks for the coming periods.Earnings Season Scorecard and This Week’s Earnings ReportsThrough all the results that came out on Friday, August 2nd, we have seen Q2 results from 456 S&P 500 members, or 91.2% of the index’s membership. Total earnings for these index members are up +9.1% from the same period last year on +5.3% higher revenues, with 79.6% beating EPS estimates and only 59% able to beat revenue estimates.Plenty of Q2 results are still to come, even though we have seen results from more than 90% of S&P 500 members already. This week brings in results from more than 400 companies, including 8 S&P 500 members. The notable companies on deck to report results this week include the aforementioned Walmart and Home Depot, Brinker International, Cisco Systems, Tapestry, Deere & Company, China’s Alibaba, Applied Materials, and others. The comparisons charts below put the earnings and revenue beats percentages for these companies in a historical context.

Image Source: Zacks Investment ResearchThe one notable feature of the above comparison charts is the very low level of Q2 revenue beats percentage. In fact, the Q2 revenue beats percentage of 59% is a new low for this group of index members over the preceding 20-quarter period (5 years). Revenue beats have been low from the start of the reporting cycle, a trend that will carry through to the end of the earnings season.The comparison charts below put the Q2 earnings and revenue growth rates for these companies in a historical context.

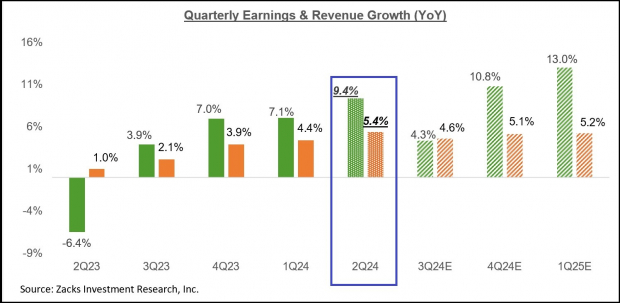

Image Source: Zacks Investment ResearchThe Earnings Big PictureLooking at Q2 as a whole, combining the actual results that have come out already with estimates for the still-to-come companies, total S&P 500 earnings are expected to be up +9.4% from the same period last year on +5.4% higher revenues.This is the highest earnings growth pace in the last eight quarters since the +10% in 2022 Q1. The Q2 aggregate earnings total is on track to be a new all-time quarterly record, as the chart below shows.

Image Source: Zacks Investment ResearchThe chart below that shows the year-over-year earnings and revenue growth for 2024 Q2 in the context of what we saw in the preceding four periods and what is currently expected for the following three periods.

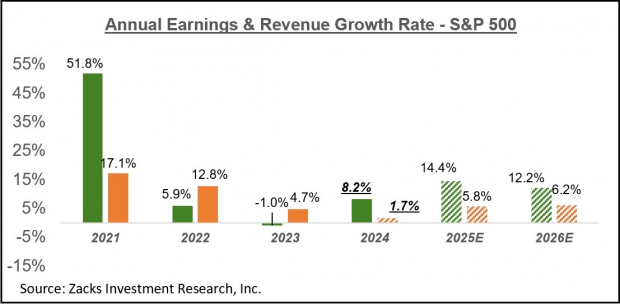

Image Source: Zacks Investment ResearchFor the current period (2024 Q3), total S&P 500 earnings are expected to be up +4.3% from the same period last year on +4.6% higher revenues.Please note that estimates for Q3 have been steadily coming down, with the current +4.3% earnings growth rate down from +6.9% in early July.This is a bigger cut to estimates relative to what we saw in the comparable periods for the preceding two quarters. The negative revisions trend is broad-based, with estimates for 14 of the 16 Zacks sectors getting cut since the quarter got underway. The biggest cuts have been to the Transportation, Business Services, Energy, Aerospace, and Basic Materials sectors. On the positive side, estimates for the Tech sector are going up, while the same for the Finance sector are only marginally higher relative to where we started in early July.Looking at earnings expectations on an annual basis, total 2024 S&P 500 earnings are expected to be up +8.2% on +1.7% revenue growth. Excluding the Energy sector drag, whose earnings are now expected to be down -11.1% in 2024, total earnings for the rest of the index would be up +9.8%.The expected 2024 revenue growth pace improves to +4.1% once Finance is excluded from the aggregate data, with the index level aggregate earnings growth for the year declining only to +7.9% on an ex-Finance basis.

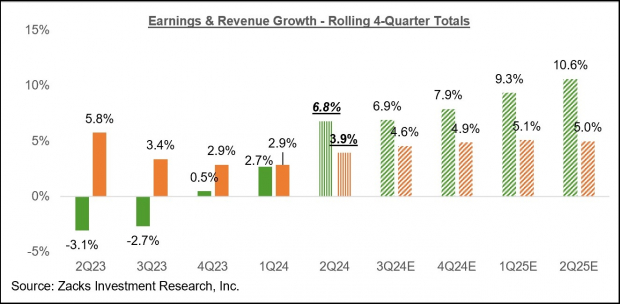

Image Source: Zacks Investment ResearchUnlike the calendar year view that the above chart shows, the chart below the earnings data on a rolling four-quarter basis

Image Source: Zacks Investment ResearchMore By This Author:Top Stock Reports For Mastercard, AMD & IntuitA Closer Look At The Current Earnings Picture Top Analyst Reports For AstraZeneca, TotalEnergies & ConocoPhillips