Talking heads and politicians laud the “resilience” of American consumers. They managed to keep spending despite rapidly rising prices thanks to post-pandemic price inflation.But these pundits and politicos rarely talk about how Americans have weathered the inflationary storm. When you look at the big picture, it’s not a story of resilience but one of desperation.In a nutshell, Americans blew through their savings and now they’re running up their credit cards.The personal savings rate plummeted in July, dropping to 2.9 percent. That was down from 3.1 percent the prior month. It was the lowest savings rate since the COVID crash.The current savings rate is roughly in the same ballpark as it was just before the Great Recession, as you can see from this graph courtesy of ZeroHedge.

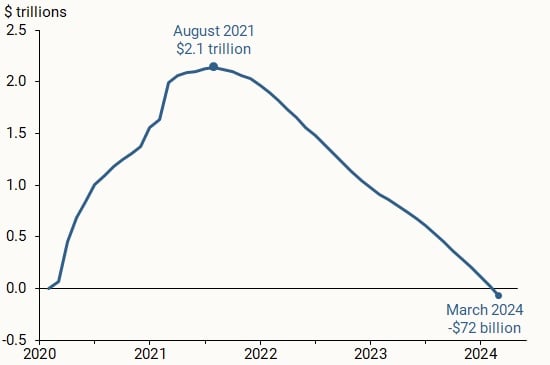

“Households drew down their excess savings at an average pace of $70 billion per month since September 2021, although this drawdown accelerated to about $85 billion per month since last fall relative to the average pace for the entire period.”

Now what? Enter Visa and Mastercard.With savings depleted, consumers turned to credit cards.Americans not only saved money during the pandemic, but they also used their stimulus checks to pay down credit card balances. Revolving credit dipped below $1 trillion during the pandemic period. But as prices started rising in the wake of COVID, Americans turned to plastic. Revolving debt currently stands at a record of $1.36 trillion. And Americans continue to use credit cards despite interest rates as high as 28 percent. In July, non-revolving credit, primarily made up of credit card balances, surged by 9 percent ($10.6 billion).Some pundits claim that increasing credit card debt is a good sign. They claim American consumers are “confident” and therefore willing to buy on credit. But spending patterns tell a different story. Citigroup recently noted that more and more consumers are using credit cards to pay for “basic needs,” and there has been a notable slowdown in “non-vital” purchases.In other words, people are using credit cards with 28 percent interest rates to pay for groceries. This isn’t the behavior of a “resilient” consumer. These are desperate consumers trying to keep pace with rising prices. This is a looming problem for a country that depends on consumers buying stuff to keep plodding along. What happens when Americans hit their credit card limits?Something to keep in mind as you hear government officials and their cheering section in the media trumpeting the “soft landing” narrative.More By This Author:American Consumers Spending More, Getting Less

What Happens When The Chinese Jump Back Into This Gold Bull Market?

Biden Administration Runs Biggest Deficit Of The Year In August