Strong Returns in STRs as an Institutional Investment, but Capital Is Still on the Sidelines

There are 1.5 million short-term vacation rentals (STRs) in the United States, out of 140 million total homes. In other words, there is one vacation home for every 116 permanent homes. While this level of market saturation may seem high, consider that the vast majority of these assets are run for personal use and not as investments.Investment capital has not yet penetrated this asset class in any meaningful way. We estimate that only 3-5% of the entire 1.5 million STR homes in the country are professionally-optimized and run for investors to maximize profits. This presents a huge opportunity for early-adopter large investors.We call these professionally-managed and optimized STR assets “Investment Grade.” We believe that STRs are one of the most compelling asset classes in real estate, given their inherent high yields, durable assets, pricing power, and inflation-hedging characteristics.

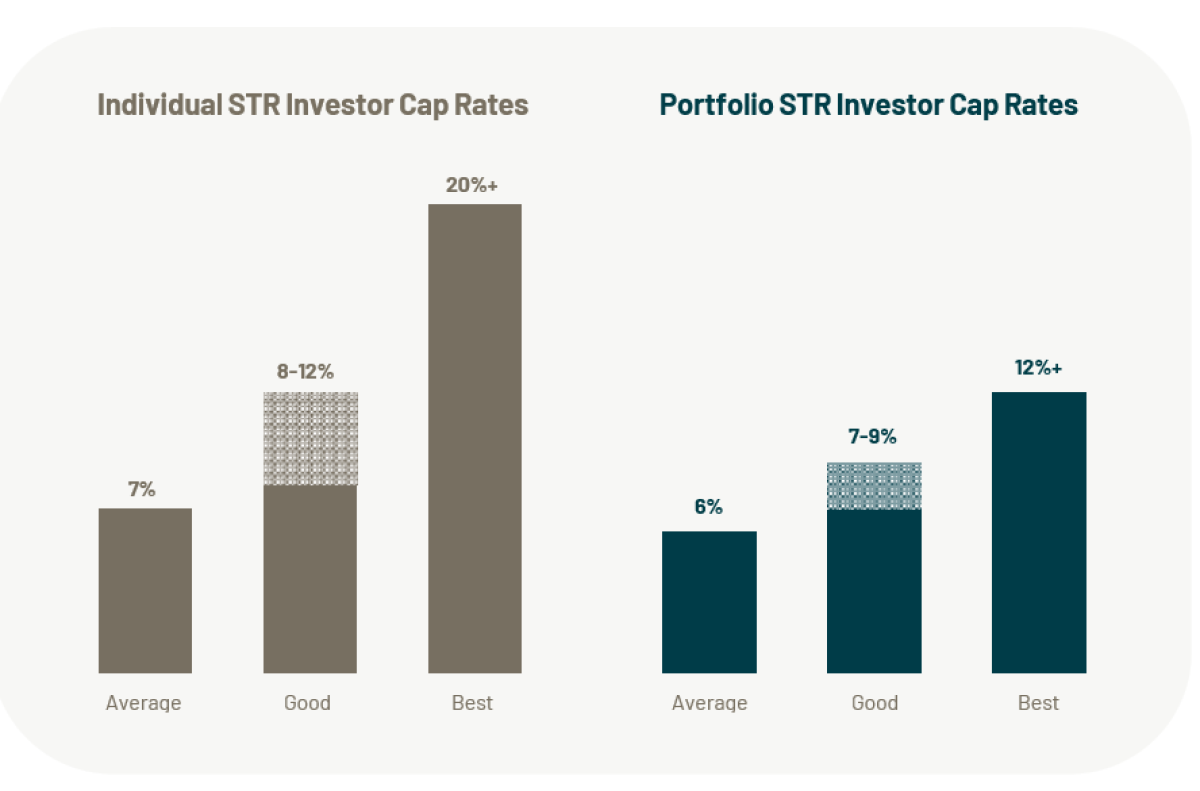

Why STRs Are the Nicest House on the Block

High returns and cash flows are typically the most exciting part of owning STR assets. In the table below, we highlight some data on STR assets that we have recently underwritten for investors and professional asset managers who purchase STRs for purely investment purposes. As you can see in the prior chart, the cap rates for those who purchase STRs for investment purposes are strong. However, initial cap rates are only part of the story. It is not uncommon to find double digit ADR/pricing growth over the past several years in many locations. Investing in the right markets to capture organic pricing growth and high localized inflation can dramatically improve returns, particularly over long-term investment horizons.

As you can see in the prior chart, the cap rates for those who purchase STRs for investment purposes are strong. However, initial cap rates are only part of the story. It is not uncommon to find double digit ADR/pricing growth over the past several years in many locations. Investing in the right markets to capture organic pricing growth and high localized inflation can dramatically improve returns, particularly over long-term investment horizons.

Enhanced Returns from Investing in Overlooked Areas

Investors can typically find more impressive returns in overlooked vacation areas. We have underwritten several portfolios with cap rates greater than 20% over the past quarter.Conversely, certain areas of the country are over-saturated with STRs, i.e. Southern California where vacation homes are purchased more for personal use than for investments, resulting in marginal or even negative cash flows. Similarly, we see crowding of institutional capital in more common vacation destinations like certain mountain/ski areas and parts of the Southeast.

But Aren’t STRs Risky?

We will address STR risk extensively in future white papers, but here we will begin with the three forms of risk that most often concern STR investors.

Cash Flow Variability

Regarding financial risks, most investors principally focus on cash flow variability. However, the right mitigating measures can smooth out or de-risk portfolios, whether that means diversifying across seasonality or installing master lease agreements.Regardless, we view pricing growth and higher cash flow yields of 30-40% as strong compensation for a bit more income statement variability. In fact, daily repricing actually empowers investors to take advantage of inflation.

Regulatory Risk

Understanding local regulations is essential for any STR investor. While no one can predict the future of restrictive regulations with perfect accuracy, thorough research and education can help mitigate risk. We not only underwrite the applicable regulations of each individual asset, but provide ongoing, forward-looking regulatory monitoring to assess the likelihood and risk of detrimental regulatory changes in each given market.

Higher Operational Complexity

For even experienced real estate investors who are most comfortable with “set it and forget it” long-term leases, the day-to-day operations of an STR may feel daunting. However, the majority of operational risks can be diluted with the right professional property manager.Finally, as we will highlight in a subsequent white paper, STR assets have strong inflation- hedging characteristics, which help offset risk. Overall, STR risk is a complex subject with a series of trade-offs, compared to other real estate and hospitality assets. However, we find their overall risk/return to be compelling.

STRs Are Still a “Niche” Investment Class

While investing equity in STR assets offers a high return, they are primarily financed with debt. We have spoken to countless lenders and investors who are struggling with debt financing options.Most lenders primarily consider the asset value of the home and not the cash flows of the STR business. Of those who do lend on cash flows, many are forced to underwrite the assets like long-term rentals because that is what is familiar and accepted in secondary markets. The industry is also lacking portfolio financing options.The lack of financing options is holding back larger pools of capital from entering the space and preventing portfolio owners and Vacation Rental Managers from consolidating at an adequate pace. Over time, we believe that innovation in debt financing will catch on to the STR opportunity, but for now, those who can entrepreneurially source debt capital are well positioned.

STR Investment Strategies

One of the more interesting aspects of STRs emerging as an asset class is their proclivity for creative investment strategies. ‘Plain vanilla’ strategies that deploy capital by geography, VRM-backed investments, type of property, etc, are still in the early innings of investment. Others are beginning to develop proprietary strategies around built-for-purpose, emerging markets, distressed properties, and more.

About the Author

Liz Marie is an award-winning strategist specializing in alternative investments. Over the last 16 years, Liz has worked with hundreds of brands across every aspect of investments and real estate, including Charles Schwab, Russell Investments, Principal Funds, Kayne Anderson, Angel Oak Capital, Gurtin Capital ($38 billion municipal bond manager acquired by PIMCO), AIG and more. She is also an STR investor.Prior to joining Revedy, Liz operated her own consultancy and served as the Creative Director at Griffin Capital, a $9 billion real estate fund company acquired by Apollo in 2022. She also spent 10 years as Director of Strategy at an investment marketing firm.More By This Author:The Impact of Passive Investing on Short SellersAlternative Investments During the First Half of 2024: Diversify Your DiversifiersInvestment Migration: An Opportunity For Alternative Investors