Image Source: cveiv, iStockPhotoThis article shows how diversification can provide the opportunity to invest in a variety of risky assets — with commensurately high expected returns — but at a fraction of the total risk that an investor would endure with any single asset on its own. By investing in variety of assets that can thrive in different economic regimes, we can protect portfolios against an uncertain future.The most fundamental principle of investing is diversification. But in our experience, few investors understand what diversification means.Sure, investors typically understand that diversification means “don’t put all your eggs in one basket.” But when we probe a little deeper, it seems many investors are still confused about how diversification works in practice. They wonder, “If I’m buying something that makes money when the other is losing money, doesn’t that just give me a zero return?”We can overcome this confusion with a simple example.In Canada, we have very distinct seasons. Some months of the year are temperate and relatively dry, while other months are cold and snowy. As a result, most Canadian towns of any size have stores that sell skis and bikes.Of course, they don’t inventory both skis and bikes at the same time. Rather, in the spring they sell off all their ski related inventory and set out their bike gear, and in the fall they clear out the bike gear to make room for skis. Let’s observe a simplified example of bike sales and ski sales over several years.

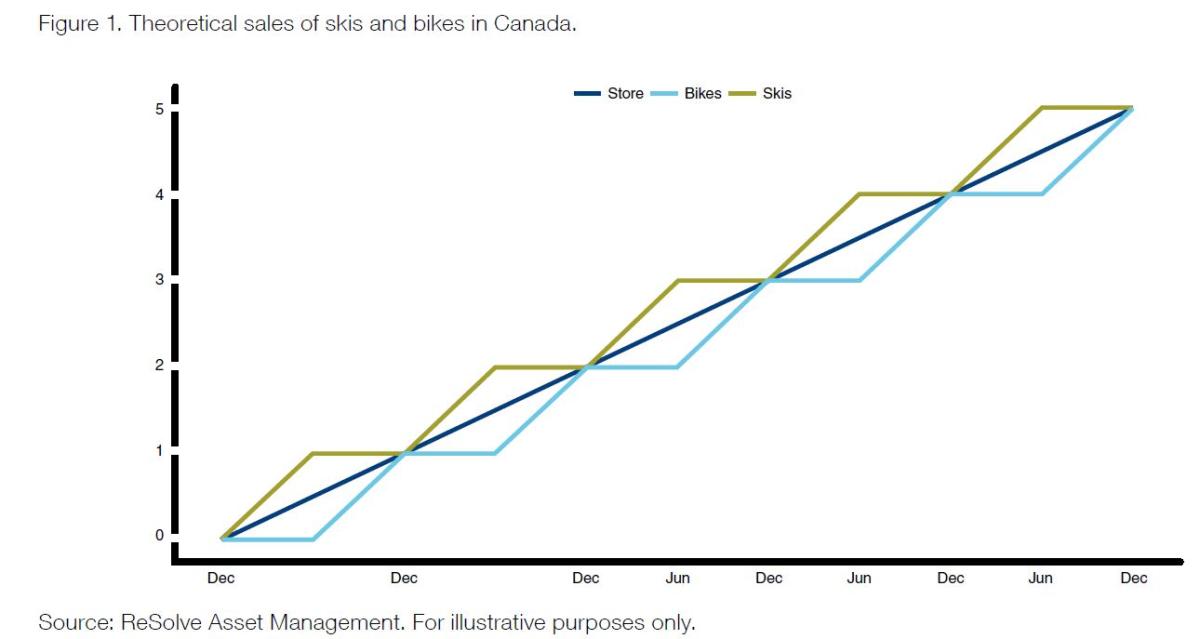

Image Source: cveiv, iStockPhotoThis article shows how diversification can provide the opportunity to invest in a variety of risky assets — with commensurately high expected returns — but at a fraction of the total risk that an investor would endure with any single asset on its own. By investing in variety of assets that can thrive in different economic regimes, we can protect portfolios against an uncertain future.The most fundamental principle of investing is diversification. But in our experience, few investors understand what diversification means.Sure, investors typically understand that diversification means “don’t put all your eggs in one basket.” But when we probe a little deeper, it seems many investors are still confused about how diversification works in practice. They wonder, “If I’m buying something that makes money when the other is losing money, doesn’t that just give me a zero return?”We can overcome this confusion with a simple example.In Canada, we have very distinct seasons. Some months of the year are temperate and relatively dry, while other months are cold and snowy. As a result, most Canadian towns of any size have stores that sell skis and bikes.Of course, they don’t inventory both skis and bikes at the same time. Rather, in the spring they sell off all their ski related inventory and set out their bike gear, and in the fall they clear out the bike gear to make room for skis. Let’s observe a simplified example of bike sales and ski sales over several years. As winter approaches, ski sales (shown by the gold line) accelerate while bike sales (shown by light blue line) drop off. As summer approaches, people stop buying skis but ramp up their purchases of bikes. The store (as sown by dark blue line) runs a steady profit all year long. This is the nature of diversification.

As winter approaches, ski sales (shown by the gold line) accelerate while bike sales (shown by light blue line) drop off. As summer approaches, people stop buying skis but ramp up their purchases of bikes. The store (as sown by dark blue line) runs a steady profit all year long. This is the nature of diversification.

Well-Executed Diversification is Indistinguishable from Magic

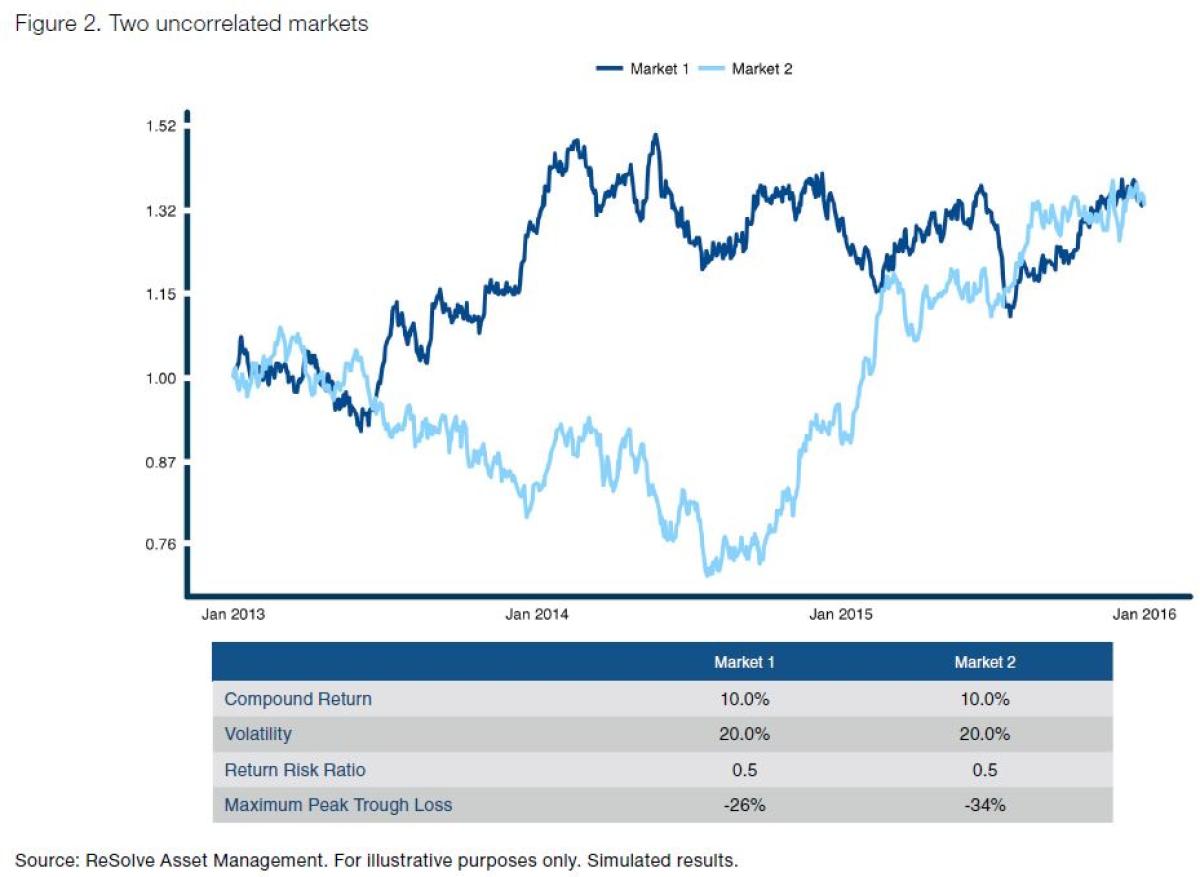

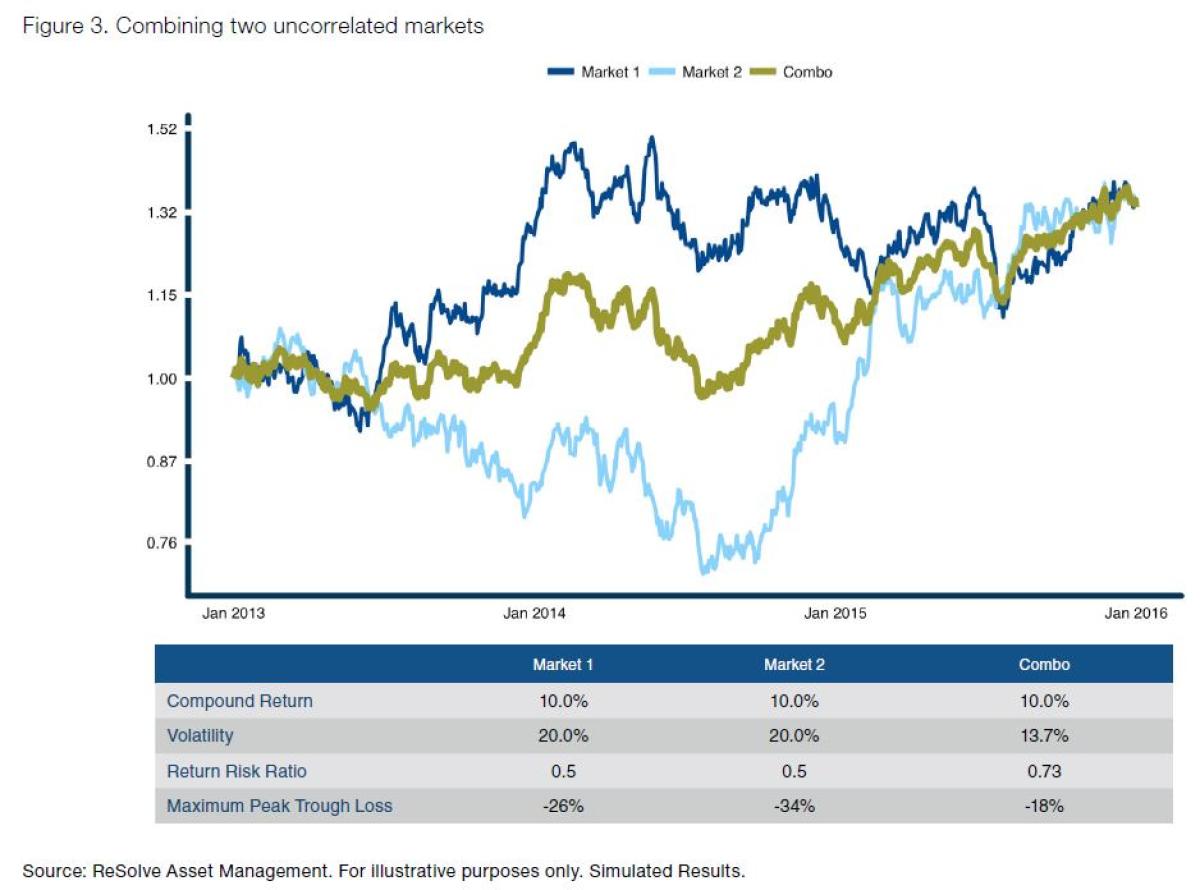

The skis and bikes example above shows how deriving cash-flows from two independently profitable businesses, which produce returns at different times, reduces the variability of cash-flows throughout the year.The skis and bikes example extends quite intuitively to the domain of investment portfolios, as well.Consider a simple example where we have two assets: Market 1 and Market 2 (see Figure 2 below). To make this example more real, assume that the markets in Figure 2 represent the returns to a long-duration bond index [Market 1] and a diversified stock index [Market 2] over the three-year period from April 2013 through March 2016. From the table below Figure 2, you will likely notice that both Market 1 and Market 2 have the same average returns over the period but achieve those returns in very different ways. In other words, they are uncorrelated assets.The lesson from our skis and bikes example above, as well as from Nobel prize winning financial theory, is that if we expect the same average outcome from both markets, and they are different, then we should take advantage of the opportunity for diversification.This is exactly what we’ve done in Figure 3 by placing half of a fictitious investor’s capital in Market 1 and half in Market 2.

From the table below Figure 2, you will likely notice that both Market 1 and Market 2 have the same average returns over the period but achieve those returns in very different ways. In other words, they are uncorrelated assets.The lesson from our skis and bikes example above, as well as from Nobel prize winning financial theory, is that if we expect the same average outcome from both markets, and they are different, then we should take advantage of the opportunity for diversification.This is exactly what we’ve done in Figure 3 by placing half of a fictitious investor’s capital in Market 1 and half in Market 2. It’s clear that diversification produces a gentler ride. While the diversified “Combo” portfolio produced the same return, it did so with about 33% less volatility.Even better, because the declines in the two markets occurred at different times, the Combo portfolio achieved its returns with a 40% smaller maximum loss than what was endured by either of the individual markets.If the concept is so clear cut, why do so few investors maximize their opportunity for diversification? Despite the clear benefits of diversification with perfect hindsight, we know from a behavioral perspective diversification can be a tough slog. To illustrate this point, lets revisit how each investor might have felt half-way through.By the mid-point in our simple example, investors who chose to diversify were probably regretting their decision, as Market 1 had produced about 25% in extra returns. Only after the completion of the period, once Market 1 experienced its own 26% decline, would diversified investors finally have felt vindicated.

It’s clear that diversification produces a gentler ride. While the diversified “Combo” portfolio produced the same return, it did so with about 33% less volatility.Even better, because the declines in the two markets occurred at different times, the Combo portfolio achieved its returns with a 40% smaller maximum loss than what was endured by either of the individual markets.If the concept is so clear cut, why do so few investors maximize their opportunity for diversification? Despite the clear benefits of diversification with perfect hindsight, we know from a behavioral perspective diversification can be a tough slog. To illustrate this point, lets revisit how each investor might have felt half-way through.By the mid-point in our simple example, investors who chose to diversify were probably regretting their decision, as Market 1 had produced about 25% in extra returns. Only after the completion of the period, once Market 1 experienced its own 26% decline, would diversified investors finally have felt vindicated.

Takeaways

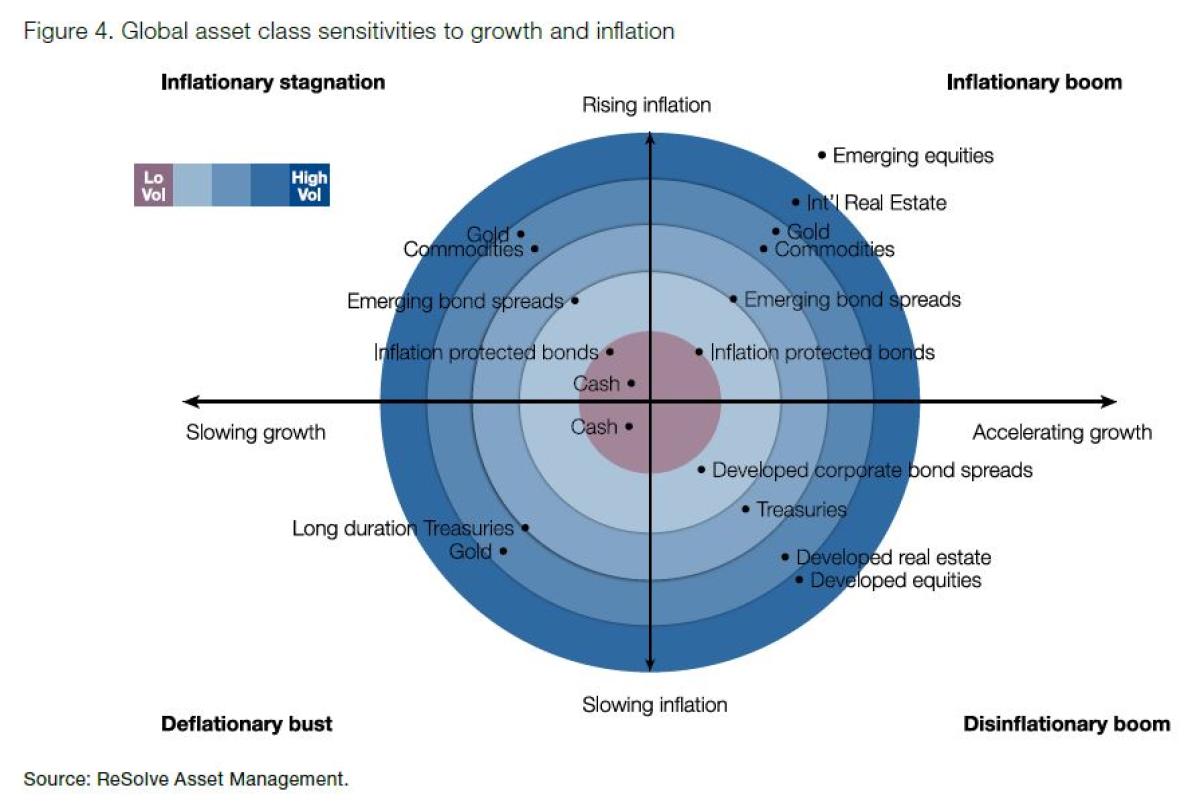

Many investors are fundamentally confused about how two assets can move in different directions without canceling each other out. Unfortunately, traditional portfolios get diversification wrong, for two reasons.First, they fail to account for the fact that asset classes have very different risk profiles. Second, most portfolios fail to invest in a diverse enough universe of asset classes that thrive in different economic states of inflation and growth. Instead, investors are conventionally overly reliant upon domestic stocks and bonds, which would only be expected to thrive in periods of sustained global growth, benign inflation, and abundant liquidity (see Figure 4 below). As previously mentioned, diversification provides the opportunity to invest in a variety of risky assets — with commensurately high expected returns — but at a fraction of the total risk that an investor would endure from an investment in any single asset on its own.We’ve yet to meet anyone with a crystal ball that can perfectly predict the future. Diversification is our greatest opportunity for protection against an uncertain future. It is paramount that investors look beyond domestic stocks and bonds into a variety of global asset classes.Much like the store that sells only skis or bikes is prepared only for one season, portfolios that rely exclusively on just domestic stocks and bonds are prepared only for one of the four major economic regimes.Diversification is therefore not only an explicit recognition that we cannot predict the future, but also a way to ensure the portfolio’s survival, regardless of what economic regime comes next.

As previously mentioned, diversification provides the opportunity to invest in a variety of risky assets — with commensurately high expected returns — but at a fraction of the total risk that an investor would endure from an investment in any single asset on its own.We’ve yet to meet anyone with a crystal ball that can perfectly predict the future. Diversification is our greatest opportunity for protection against an uncertain future. It is paramount that investors look beyond domestic stocks and bonds into a variety of global asset classes.Much like the store that sells only skis or bikes is prepared only for one season, portfolios that rely exclusively on just domestic stocks and bonds are prepared only for one of the four major economic regimes.Diversification is therefore not only an explicit recognition that we cannot predict the future, but also a way to ensure the portfolio’s survival, regardless of what economic regime comes next.

About the Author

Rodrigo Gordillo, CIM is President & Portfolio Manager of ReSolve Asset Management SECZ and has over 16 years of experience in investment management.He has co-authored the book Adaptive Asset Allocation: Dynamic Global Portfolios to Profit in Good Times – and Bad (Wiley), as well several whitepapers and research focused on adding new insights to the quantitative global asset allocation space. Rodrigo began his career on the institutional side with John Hancock before transitioning to the ultra-high net worth space at one of the largest boutique wealth management firms in Toronto.Subsequently, Rodrigo continued to evolve his quantitatively focused investment methodology as a Portfolio Manager at Macquarie Canada and Dundee Goodman before launching ReSolve Asset Management Inc (Canada) in 2015 and ReSolve Asset Management SEZC (Cayman) in 2019.More By This Author:What Does A Once-In-A-Generation Investment Opportunity Look Like?The Distribution Of Stock Market ReturnsCredit Hedging Done Right: CDX Outperforms with Defense