Image: BigstockEnphase Energy Inc. (ENPH – Free Report) recently revealed that its Solargraf software now comes with a new artificial intelligence (AI)-powered do-it-yourself (DIY) permitting feature for its customers in the United States. This DIY feature boasts the capability to automate the complex solar and battery permitting process and can thus help lower solar permit plan creation time by up to 95%.The new DIY permit plan feature transforms the Solargraf platform into a complete end-to-end solution for solar and battery system design, proposal generation, and permitting. This new feature not only optimizes installers’ productivity, but also lowers costs by minimizing cycle times and operating expenses through an efficient, automated workflow.The Solargraf platform, with its new DIY permitting feature, is expected to empower solar installers to operate more efficiently, which, in turn, might lure solar investors to add the stock to their portfolio. However, to assert if it would be profitable to add this to your portfolio right now or wait a little longer, let’s delve deeper into the stock’s year-to-date performance, long-term prospects, as well as risks (if any) to investing in the stock. The idea is to help investors make a prudent decision.

Image: BigstockEnphase Energy Inc. (ENPH – Free Report) recently revealed that its Solargraf software now comes with a new artificial intelligence (AI)-powered do-it-yourself (DIY) permitting feature for its customers in the United States. This DIY feature boasts the capability to automate the complex solar and battery permitting process and can thus help lower solar permit plan creation time by up to 95%.The new DIY permit plan feature transforms the Solargraf platform into a complete end-to-end solution for solar and battery system design, proposal generation, and permitting. This new feature not only optimizes installers’ productivity, but also lowers costs by minimizing cycle times and operating expenses through an efficient, automated workflow.The Solargraf platform, with its new DIY permitting feature, is expected to empower solar installers to operate more efficiently, which, in turn, might lure solar investors to add the stock to their portfolio. However, to assert if it would be profitable to add this to your portfolio right now or wait a little longer, let’s delve deeper into the stock’s year-to-date performance, long-term prospects, as well as risks (if any) to investing in the stock. The idea is to help investors make a prudent decision.

Enphase Energy Stock Lags Industry, Sector, & S&P 500

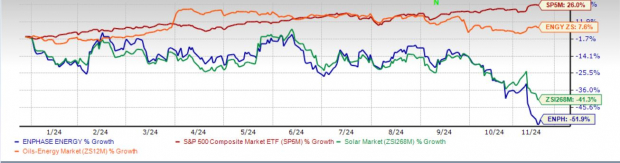

Enphase Energy’s shares have lost 51.9% in the year-to-date period, underperforming the Zacks Solar industry’s decline of 41.3% as well as the broader Zacks Oil-Energy sector’s growth of 7.6%. The stock also lagged the S&P 500’s surge of 26% in the same period.A similar dismal performance has been delivered by other industry players, such as Emeren Group (SOL – Free Report), Sunrun (RUN – Free Report), and SolarEdge Technologies (SEDG – Free Report), whose shares have lost 30.1%, 44.4%, and 86.3%, respectively, year-to-date.

Enphase Energy Year-to-Date Performance

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

What Led to Enphase Energy Stock’s Downfall?

Enphase Energy has been persistently suffering in recent times due to the dismal demand environment in the United States and Europe. Such a sluggish demand trend has been adversely impacting the company’s product sales and, thereby, its operational results. This is further evident from the company’s poor third-quarter 2024 results despite it being a prominent U.S. solar microinverter manufacturer.The company’s third-quarter revenues plunged 30.9% year-over-year, primarily due to a 56% decline in microinverter shipment. In fact, the company has been delivering such dismal operating performance for the past couple of quarters, which must have led to the notable year-to-date decline in its share price.

Will Enphase Stock Recover?

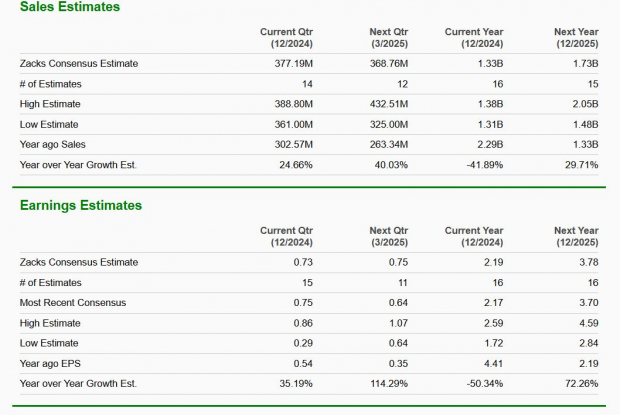

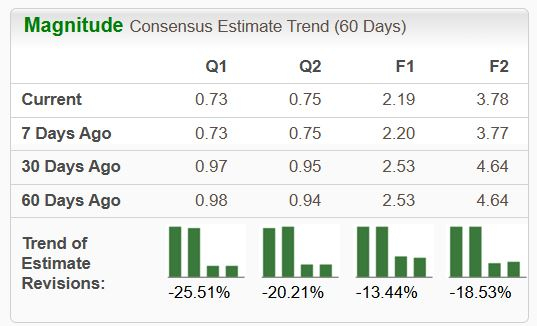

Although some improvements have been witnessed in the demand scenario in the United States and Europe lately, the overall impact is not going to disappear any time soon. However, with the U.S. Central Bank having lowered the interest rate for the nation after a long time, the downward pressure on Enphase Energy’s bottom line might be relieved to some extent for the time being. So, the near-term expectations for Enphase’s operating results reflect mixed sentiments.The Zacks Consensus Estimate for the stock’s fourth-quarter 2024 revenues and earnings indicates an improvement of 24.7% and 35.2%, respectively, from the prior-year quarter’s reading.However, the top and bottom-line estimates for 2024 mirror a disappointing picture. Moreover, the downward revision in its earnings estimate implies investors’ declining confidence in this stock. On a brighter note, the consensus estimate for Enphase’s long-term earnings growth rate is 9.7%. The consensus mark for 2025 earnings implies solid growth prospects. So, we may expect the stock to recover from its current ordeal in the coming years. Image Source: Zacks Investment Research

Image Source: Zacks Investment Research Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Enphase Energy Trading at a Premium

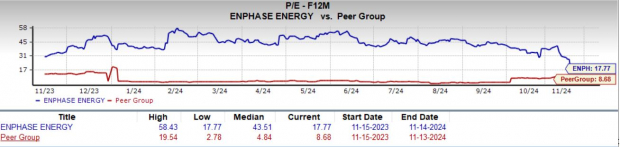

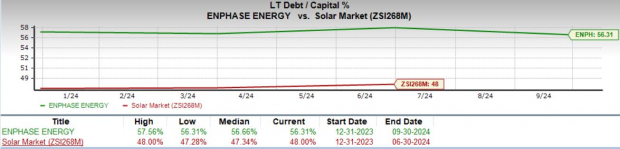

In terms of valuation, Enphase’s forward 12-month price-to-earnings (P/E) is 17.77X, a premium to its peer group’s average of 15.57X. This suggests that investors will be paying a higher price than the company’s expected earnings growth compared to that of its peer group. Image Source: Zacks Investment ResearchRisks to Consider Before Buying Enphase EnergyThe global supply market for semiconductors, integrated circuits, and other electronic components used in some of Enphase’s products has recently experienced significant constraints and disruptions. This constrained supply environment has adversely impacted and could further affect component availability, lead times, and costs. It might also increase the likelihood of unexpected cancellations or delays in the previously committed supply of key components for the company.In the United States, Enphase Energy has been witnessing a demand slowdown due to higher interest rates, high channel inventory and the transition from Net Energy Metering 2.0 (“NEM 2.0”) to Net Energy Metering 3.0 (“NEM 3.0”) in California, which increased the payback period for Enphase Energy’s customers in the state.In Europe, the company faced a slowdown on account of softer customer demand as utility rates dropped and policy changes were implemented. The company expects some of these challenges to continue to affect its operational results in the near-term, which, in turn, is likely to have an adverse impact on its fourth-quarter and full-year 2024 results. Moreover, Enphase Energy is highly debt-ridden, as evident from its long-term debt-to-capital ratio of 56.31X, which is much higher than its industry’s 48X.

Image Source: Zacks Investment ResearchRisks to Consider Before Buying Enphase EnergyThe global supply market for semiconductors, integrated circuits, and other electronic components used in some of Enphase’s products has recently experienced significant constraints and disruptions. This constrained supply environment has adversely impacted and could further affect component availability, lead times, and costs. It might also increase the likelihood of unexpected cancellations or delays in the previously committed supply of key components for the company.In the United States, Enphase Energy has been witnessing a demand slowdown due to higher interest rates, high channel inventory and the transition from Net Energy Metering 2.0 (“NEM 2.0”) to Net Energy Metering 3.0 (“NEM 3.0”) in California, which increased the payback period for Enphase Energy’s customers in the state.In Europe, the company faced a slowdown on account of softer customer demand as utility rates dropped and policy changes were implemented. The company expects some of these challenges to continue to affect its operational results in the near-term, which, in turn, is likely to have an adverse impact on its fourth-quarter and full-year 2024 results. Moreover, Enphase Energy is highly debt-ridden, as evident from its long-term debt-to-capital ratio of 56.31X, which is much higher than its industry’s 48X. Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Final Thoughts

To summarize, it is not advisable to add this stock to one’s portfolio right now, considering its premium valuation, dismal year-to-date performance, and high leverage. Nevertheless, those who already own this Zacks Rank #3 (Hold) company’s shares may continue to do so, considering its long-term growth prospects.More By This Author:Why CyberArk Stock Is A Standout After Q3 Earnings This Week5 Defensive Stocks To Counter Volatility As Post-Election Rally HaltsTime To Buy Home Depot Or Disney Stock After Beating Earnings Expectations?