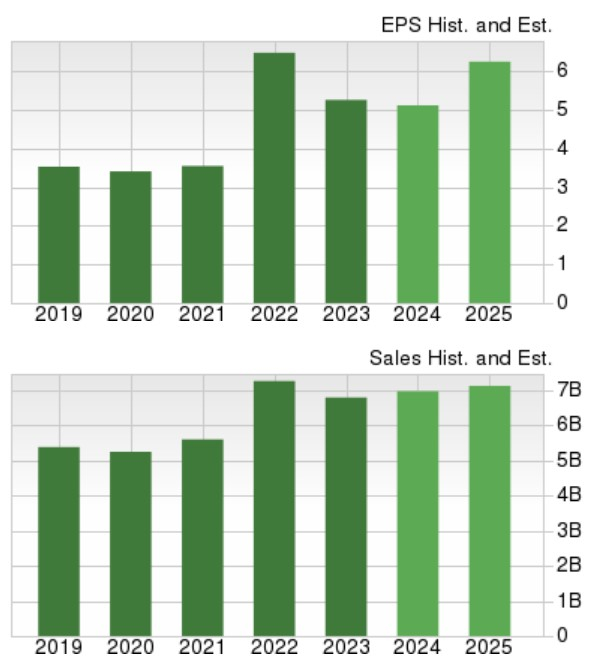

Investors looking for shares of a company that has the remnants of a value stock and growth potential may want to consider Sonoco Products (SON).With its incorporation dating back to 1899, Sonoco has become a leading provider of consumer packaging, industrial products, protective packaging, and packaging supply chain services.Headquartered in Hartsville South Carolina, now appears to be an ideal time to buy stock in this historic American company with SON sporting a Zacks Rank #1 (Strong Buy) and landing the Bull of the Day. Q4 Expectations & FY25 ProjectionsSet to release its fourth-quarter results on February 18, Sonoco’s Q4 earnings are expected to increase 20% to $1.23 per share. This is despite Q4 sales forecast of $1.57 billion compared to $1.64 billion in the comparative quarter. Speaking to Sonoco’s operational efficiency, the company is effectively navigating a weaker business environment and has started to stand out amongst its closest competitors such as Graphic Packaging Holding Company (GPK) and Sealed Air (SEE) .Correlating with such, Sonoco’s EPS is now expected to dip 2% as the company rounds out fiscal 2024 but is projected to rebound and spike 19% in FY25 to $6.11 per share. Total sales are thought to have dipped 4% in FY24 but are expected to stabilize and soar 35% this year to $8.78 billion.

Image Source: Zacks Investment Research Sonoco’s Attractive ValuationMaking FY25 rebound projections more appealing is that Sonoco’s stock trades at just 7.8X forward earnings compared to its Zacks Containers-Paper and Packaging Industry average of 15X.Furthermore, SON trades nicely beneath its decade-long high of 19.9X forward earnings and is at a sharp discount to the median of 16.3X during this period.

Image Source: Zacks Investment ResearchSON is also at the optimum level of less than 2X sales (0.7X) and its PEG ratio of 0.7 further suggests the company is undervalued when considering its growth rate.

Image Source: Zacks Investment Research Sonoco’s Enticing Dividend1. Sonoco currently has a very generous 4.26% annual dividend yield which impressively tops its industry average of 2.64%.2. Another dividend hike should be expected in 2025 as Sonoco is not a member of the S&P 500 but would have the classification of a Dividend Aristocrat after increasing its dividend for more than 25 consecutive years (34).3. Sonoco’s 42% payout ratio indicates there is plenty of room to raise its dividend in the future.

Image Source: Zacks Investment Research Bottom LineSonoco is one of the more intriguing stocks to watch leading up to its Q4 report, and in addition to its strong buy rating has an overall “A” VGM Zacks Style Scores grade for the combination of Value, Growth, and Momentum.More By This Author:Meta Vs Microsoft: Which Stock Is More Attractive Ahead Of Earnings? Tesla Earnings Preview: The Best Of The Mag 7?3 Instruments Stocks Likely To Beat Short-Term Industry Hardships