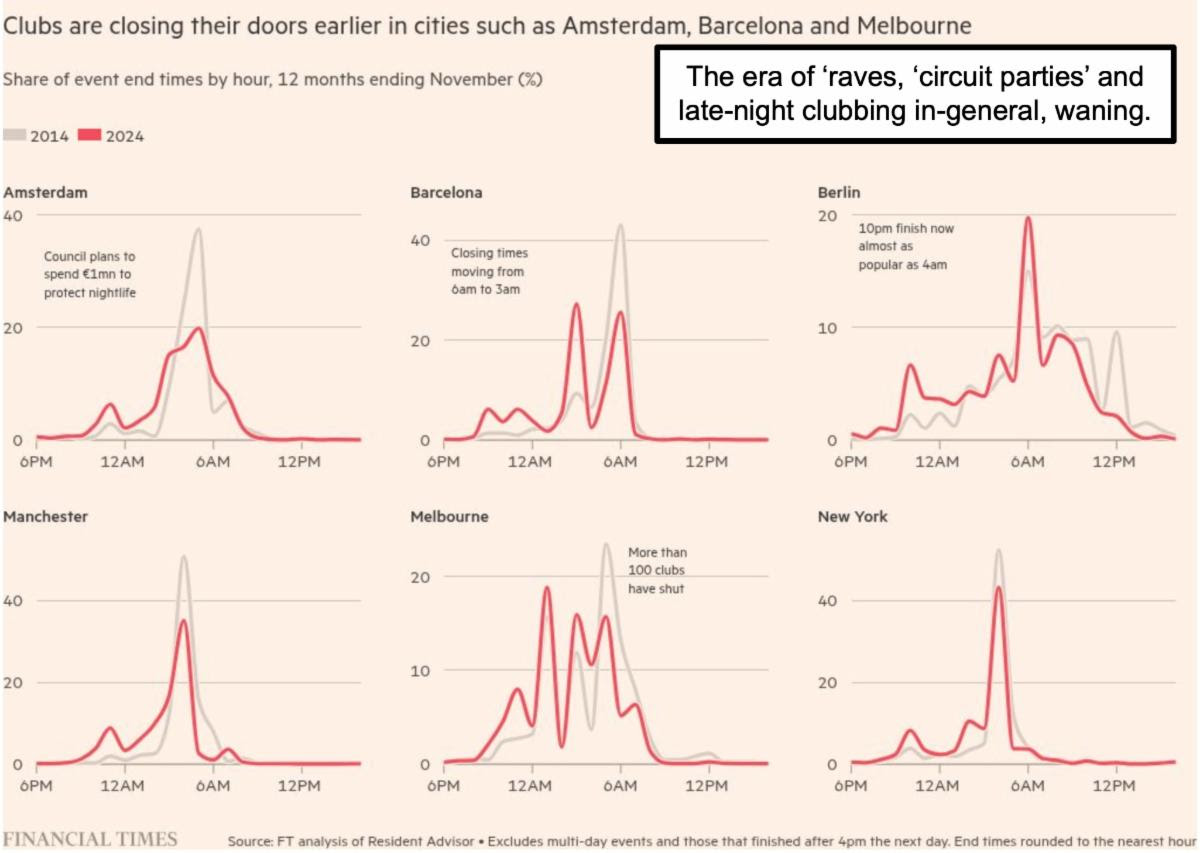

A sloppy transition from the old year to a new one engendered enough of a risk fear, that it helped increase shorting ‘and’ (for a number of stocks), did one more thing: it let Market-Makers distribute; drop stocks to absorb supply, and thus ‘rebuild inventory’, which contributed to feeding late week recovery.In the House, Speaker Johnson managed to retain his ‘speakership’ after just failing narrowly on the 1st vote. No second vote needed, as he just cajoled a couple members into changing their votes. No nonsense going forward there.Just for kicks, the graphic below reflects not just less interest in partying; just drinking; or lack of money for extremely unessential spending; but also might reflect security concerns, as all these cities (among others) have witnessed a lot of incidents, barbarian Islamic terror, or quasi-terrorist protests. So people are staying home more; although the era of big clubs gave-way to ‘wine bars’ and smaller lounges, over a period of years. And where clubs operate; many are finally closing at earlier hours (if you haven’t found whatever by 2 am. just give it a rest I’d say.. hah .. says the way ‘over the hill’ never club kid guy). So much for post-holiday reflection; as we get ready for the other party..Trump. Many on Wall Street expect ‘day one’ of Trump 2.0 will reinforce ‘deregulation; which is one of the primary factors that’s holding-up big-cap stocks generally; at the same time it’s even more important in the (concentrated) big-cap techs. I’m not particularly optimistic on S&P or Indexes; while very optimistic on ‘new era’ digital stocks, some of which have spent months for their day in the sun.As to believing the market is overly ‘Pollyannish’ … I’d say that was the big-cap or ‘magnificent seven’ case just a month ago; but not so much now. The focus of many money managers seemingly ‘finally’ embraced our view of ‘shaving’ a bit of the mega-tech gains and shifting into ‘Application Software’ tickers; that have smaller-cap opportunities too; not just the obvious behemoth leaders.

Many on Wall Street expect ‘day one’ of Trump 2.0 will reinforce ‘deregulation; which is one of the primary factors that’s holding-up big-cap stocks generally; at the same time it’s even more important in the (concentrated) big-cap techs. I’m not particularly optimistic on S&P or Indexes; while very optimistic on ‘new era’ digital stocks, some of which have spent months for their day in the sun.As to believing the market is overly ‘Pollyannish’ … I’d say that was the big-cap or ‘magnificent seven’ case just a month ago; but not so much now. The focus of many money managers seemingly ‘finally’ embraced our view of ‘shaving’ a bit of the mega-tech gains and shifting into ‘Application Software’ tickers; that have smaller-cap opportunities too; not just the obvious behemoth leaders. Market X-ray: we have suggested that the very late-year big-cap shakeouts, leading to the slightly rough start to the New Year, would actually be a plus.Besides letting tax adjustments take place, Market Makers have been able to reload inventory as well as institutions start nibbling especially in new names for them, with bloated big-caps not as attractive; though some will do fine. At least investors had some price concession; as I termed the dips generally an opportunity to get into certain tickers, not out of. There is no change in views.One key will be security & affordability issues; this incoming Administration is spot-on focused on that even more so than the prior. Affordable will make it a challenge for the ‘biggest Defense contractors; not always favor the smaller; but possibly increase M&A activity during the year. New IPO’s will influence this too (like Anduril), while small companies popular with Law Enforcement, Border Control and Trump 1.0 (I am particularly thinking of Airship).I’m also thinking about KULR, because it’s anti-vibration system means a lot for helicopters and drone stability; but also SpaceX (and they should do well if they focus on actual business and less so on their Bitcoin treasury venture).

Market X-ray: we have suggested that the very late-year big-cap shakeouts, leading to the slightly rough start to the New Year, would actually be a plus.Besides letting tax adjustments take place, Market Makers have been able to reload inventory as well as institutions start nibbling especially in new names for them, with bloated big-caps not as attractive; though some will do fine. At least investors had some price concession; as I termed the dips generally an opportunity to get into certain tickers, not out of. There is no change in views.One key will be security & affordability issues; this incoming Administration is spot-on focused on that even more so than the prior. Affordable will make it a challenge for the ‘biggest Defense contractors; not always favor the smaller; but possibly increase M&A activity during the year. New IPO’s will influence this too (like Anduril), while small companies popular with Law Enforcement, Border Control and Trump 1.0 (I am particularly thinking of Airship).I’m also thinking about KULR, because it’s anti-vibration system means a lot for helicopters and drone stability; but also SpaceX (and they should do well if they focus on actual business and less so on their Bitcoin treasury venture). This year is in the process of sorting out its focus; but much of that is maturing in areas that were already formatively higher; including Quantum Computing stocks that (of course) Wall Street will like more as they get more expensive. I am not changing any of my views on those, while watching for developments.

This year is in the process of sorting out its focus; but much of that is maturing in areas that were already formatively higher; including Quantum Computing stocks that (of course) Wall Street will like more as they get more expensive. I am not changing any of my views on those, while watching for developments. Bottom-line: we’re not at reasonable multiples for S&P; large-cap growth not so great; too popular; very pricey; and can (but not universally) have impacts on all kinds of stocks, if they break dramatically. So far no catalyst doing that.So there’s no change as I have in mind a couple meaningful S&P declines; at the same time that may be offset somewhat by Financial or Energy strength; as well as the structural shift to digital players, which is another description of what I have simply called new-era stocks.I do understand some skepticism about ‘digital’ stocks. So yes it can be a sort of ‘Gilded Age’ for some of them (that’s partially why I’ve been more skeptical of the S&P than of hotter Quantum or AI stocks -typically software more than hardware- for a period of time). Now we have CES which may affirm or deny continued optimism (or shift to moderate enthusiasm) for a couple. We’ll see.As to the new week; not worried about the Purchasing Managers’ Index or the JOLTS survey or the Jobs number (minimal shuffling of the macro Indexes). I am less interested in ‘robots’ at CES; more in Jensen Huang’s CES Keynote about GPU, ‘drives’, and maybe we hear about ‘biometric border control’ and Aviation processing. Again, we shall see; and because NVDA etc. are in GPUs; maybe they’ll soft-pedal QPUs. (?)

Bottom-line: we’re not at reasonable multiples for S&P; large-cap growth not so great; too popular; very pricey; and can (but not universally) have impacts on all kinds of stocks, if they break dramatically. So far no catalyst doing that.So there’s no change as I have in mind a couple meaningful S&P declines; at the same time that may be offset somewhat by Financial or Energy strength; as well as the structural shift to digital players, which is another description of what I have simply called new-era stocks.I do understand some skepticism about ‘digital’ stocks. So yes it can be a sort of ‘Gilded Age’ for some of them (that’s partially why I’ve been more skeptical of the S&P than of hotter Quantum or AI stocks -typically software more than hardware- for a period of time). Now we have CES which may affirm or deny continued optimism (or shift to moderate enthusiasm) for a couple. We’ll see.As to the new week; not worried about the Purchasing Managers’ Index or the JOLTS survey or the Jobs number (minimal shuffling of the macro Indexes). I am less interested in ‘robots’ at CES; more in Jensen Huang’s CES Keynote about GPU, ‘drives’, and maybe we hear about ‘biometric border control’ and Aviation processing. Again, we shall see; and because NVDA etc. are in GPUs; maybe they’ll soft-pedal QPUs. (?) More By This Author:Market Briefing For Monday, Dec. 30, 2024

More By This Author:Market Briefing For Monday, Dec. 30, 2024

Market Briefing For Monday, Dec. 23rd

Market Briefing For Monday, Dec. 16th